Stalled trade integration and rising tariffs are testing global economic resilience

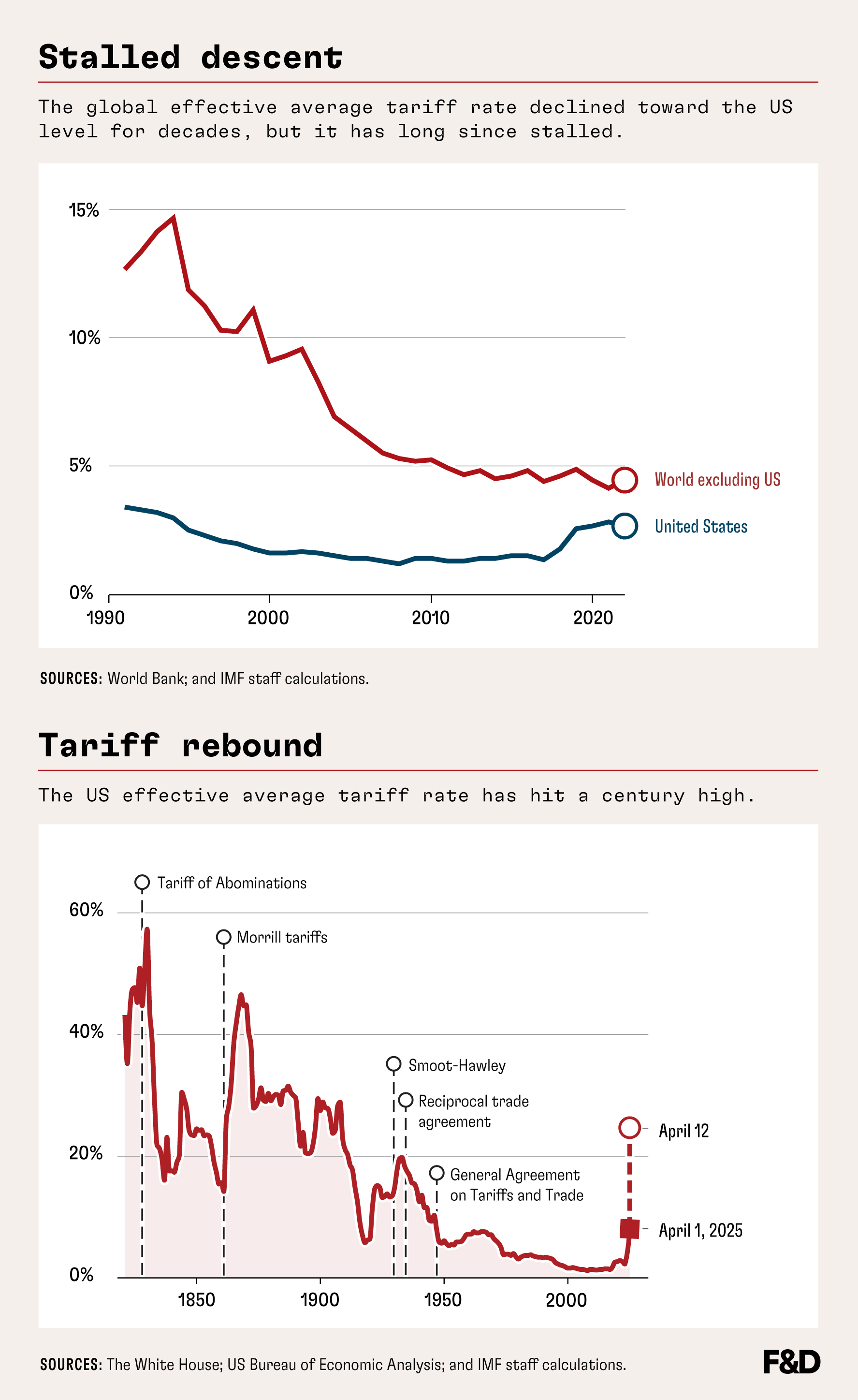

For decades, world trade expanded rapidly as countries lowered tariffs and embraced globalization. Tariff rates fell dramatically worldwide, converging toward the low levels of the United States.

But progress has stalled. Since the 2008 financial crisis, trade openness has stopped rising and global imports have leveled off at about a third of GDP. Trade tensions have escalated this year, and some major economies are reversing course, with US tariffs in April reaching the highest level in over a century. Other countries have responded.

This new trade landscape has serious consequences for the global economy. Many smaller, trade-reliant countries are more exposed to these shifts in trade patterns. Trade policy uncertainty is off the charts, making it harder for businesses everywhere to plan ahead.

The best strategy for economies to navigate uncertainty and improve growth potential is to strengthen resilience and competitiveness at home. This means fortifying macroeconomic fundamentals by rebuilding fiscal buffers, maintaining price stability, and ensuring financial soundness. Reforms to boost productivity, lower barriers to private enterprise, and attract investment can help economies adapt.

It is equally important to address internal and external imbalances, particularly large deficits and surpluses, which have contributed to the rise in tensions.

The task now is not to preserve the old but to build something new—a global economy that is more balanced and more resilient.

This article draws on an April 17, 2025, speech, “Toward a Better Balanced and More Resilient World,” by IMF Managing Director Kristalina Georgieva.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.