Countries in the Middle East and Central Asia face with COVID-19 a public health emergency unlike any seen in our lifetime, along with an unprecedented economic downturn. The pandemic is exacerbating existing economic and social challenges, calling for urgent action to mitigate the threat of long-term damage to incomes and growth.

As analyzed in our new Regional Economic Outlook, while the region responded resolutely and swiftly to save lives and stepped in with unprecedented policies to cushion the negative economic impact of containment policies, challenges abound.

While these challenges are stark and the period ahead highly uncertain, we see a path forward.

Think of the precipitous declines in oil demand and prices, which underlie our -6.6 percent growth projection in 2020 for oil exporters in the Middle East, North Africa, Afghanistan, and Pakistan (MENAP) region. Or consider the damage to trade and tourism, which is mostly offsetting the benefits from lower oil prices in MENAP’s oil importers—leading to projected growth of -1 percent for these countries. The Caucasus and Central Asia (CCA) is also impacted, with a projected contraction of -2.1 percent in 2020, driven by a significant slowdown among the region’s oil importers.

While geopolitical tensions are elevated, countries in the region are encountering falling fiscal revenues, increasing debt, higher unemployment, and rising poverty and inequality.

Looking ahead to 2021, while growth should resume in most countries, the outlook will continue to be challenging.

-

Weak oil demand and large inventories are likely to remain concerns for oil exporters, and while OPEC+ agreements helped stabilize oil prices, these are expected to remain 25 percent below their 2019 average.

-

The threat of economic scarring—long-term losses to growth, employment, and incomes—is a key concern. In particular, we estimate that five years from now countries could be 12 percent below the GDP level expected by pre-crisis trends. What’s more, for countries that depend heavily on the battered tourism sector, both baseline GDP and employment could go down by 5 percentage points this year, with effects lingering over the next 2-5 years, while poverty could rise by more than 3½ percent in 2020 if remittances do not rebound.

-

The pandemic will exacerbate the daunting challenges faced by fragile and conflict-affected states and could increase social unrest. Poor living conditions among refugees and internally displaced persons could also increase the risk of COVID-19 outbreaks.

-

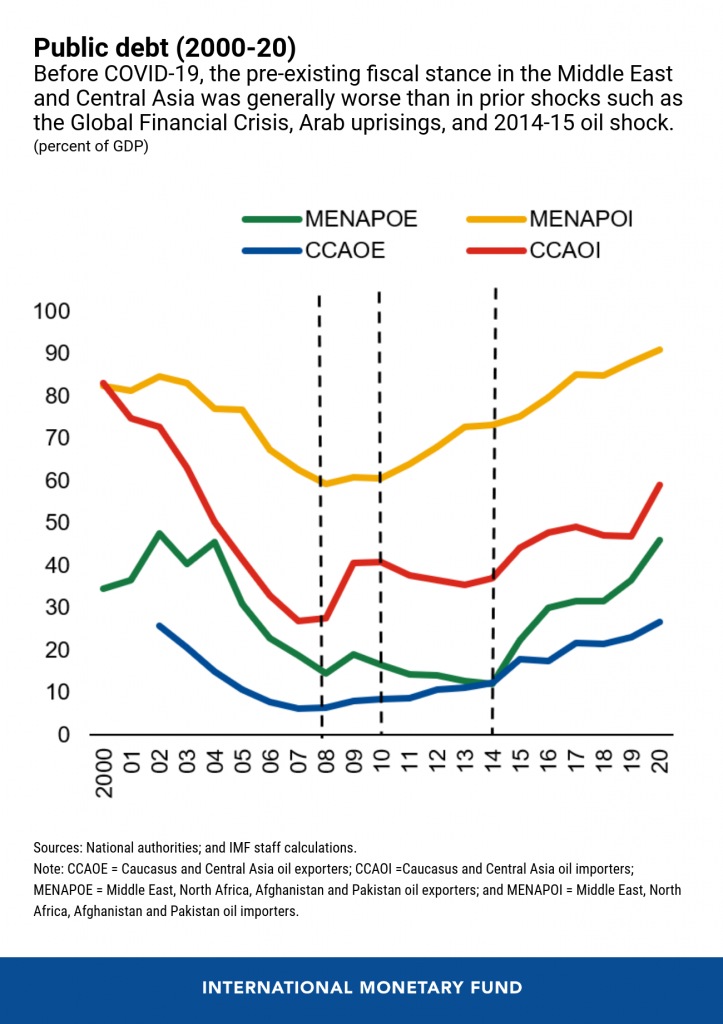

In many countries fiscal deficits and debt have increased by amounts not seen in two decades (see chart), leaving the region vulnerable to a resurgence of the virus given the likely increased spending needs and lower tax revenues. Rising deficits will also boost financing needs in the region by a median increase of 4.3 percent of GDP.

- The crisis has also heightened corporate default risk and credit risk for banks in the region, with potential losses that could amount to $190 billion or 5 percent of GDP. If unaddressed, these developments may threaten financial stability and constrain the endeavor for greater financial inclusion.

While these challenges are stark and the period ahead highly uncertain, we see a path forward. As countries continue to contain the pandemic’s toll, policymakers must increasingly turn their attention to planning and financing the recovery ahead, with a renewed focus on building greener, more inclusive, and more resilient economies.

In the immediate future, containing the pandemic and limiting income losses remain top priorities. As the public health threat begins to wane, countries should shift their focus to strengthening inclusion and addressing vulnerabilities by supporting economic activity without incurring undue risks, through well-calibrated approaches. For those with space in their budgets, such as some oil exporters, broader stimulus packages can boost demand. In countries with less space, which includes most oil importers, governments should reallocate expenditures to ensure that health, education, and social spending are protected. As the recovery gains momentum, countries should rebuild buffers and explore ways to better ensure that the tax burden is distributed fairly and that every cent of public spending delivers the best outcomes.

Ensuring all workers in the region have adequate access to health care is a critical need, particularly in oil-exporting countries with large expatriate populations. Oil exporters should also prioritize widening support for small and medium-sized enterprises and startups so that future economic prosperity is more inclusive. Accelerating economic diversification and investing in the well-educated young population will be vital, as the current crisis has illustrated. This will require fostering an institutional environment that is conducive to private sector growth—one with clear rules of the game as well as less red tape and corruption, with the public sector serving as an enabler.

Meanwhile, oil importers should permanently strengthen social safety nets and work to improve their coverage and targeting including through digital solutions. Addressing the legacies of the crisis, particularly elevated debt and weakened buffers, would underpin the recovery. Additionally, reducing many countries’ high dependence on tourism (for example, Georgia, Jordan, and Lebanon) and remittances (such as the Kyrgyz Republic, Tajikistan, Egypt, and Pakistan) will help bolster resilience to future economic shocks.

Finally, the threat posed by climate change remains the existential challenge of our time with stark implications for the region, particularly for oil exporters who will face a transformational moment for their economies. Green infrastructure investments and innovation, together with steadily rising carbon prices, will allow the region to not just fulfil its role in reducing global emissions but also to create jobs and growth for a new era.

As we face the difficult and uncertain road ahead, multilateral cooperation will be more important than ever. Working together, policymakers, nongovernmental organizations, international institutions, and citizens can build a better future.

At the IMF, we stand with the Middle East and Central Asia as it continues to save lives and begin the recovery. In addition to policy advice and technical assistance, $17 billion of new financing has been extended since the beginning of the year, including $6 billion in emergency support to 10 countries spanning both the MENAP and CCA regions. As a result, IMF’s credit outstanding to the region increased by nearly 50 percent. Our support will continue during these challenging times.

We will undoubtedly look back on 2020 as a year of suffering for far too many. But let us also remember it as a time when our region recommitted itself to building a stronger, greener, and more inclusive future.