A busy street is closed for pedestrians in São Paulo, Brazil: Economic activity picked up this year in the region, but reforms are needed to keep the positive momentum going (photo: Luciano Marques/iStock)

Latin America and Caribbean: Seizing the Momentum

May 11, 2018

Growth in Latin America and the Caribbean is picking up, thanks to stronger demand at home, and a favorable global environment helped also by rebounding commodity prices. But to secure more durable growth with widespread benefits, the region needs to invest more in key sectors, like infrastructure and education, to boost productivity over the longer-term, the IMF said in its latest regional assessment.

Stronger economic recovery

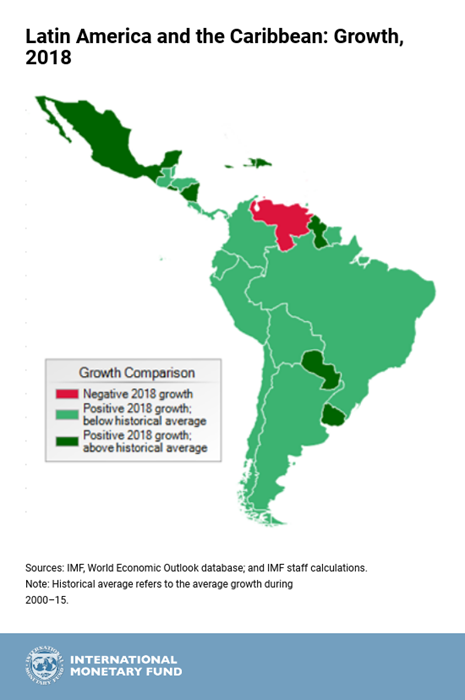

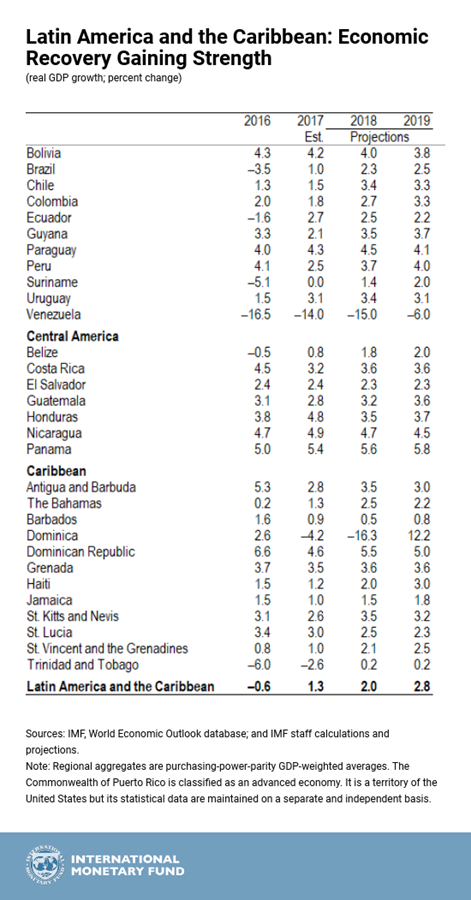

The Regional Economic Outlook for the Western Hemisphere estimates growth for the region to increase from 1.3 percent in 2017 to 2 percent in 2018. For 2019, the report forecasts growth to continue to pick up to 2.8 percent.

Following the recovery in private consumption in 2017, business investment is expected to rise and become the main driver of economic activity, after a three-year contraction.

Despite this rebound, investment levels are expected to remain below the levels as seen in other regions, limiting the region’s growth potential, according to the report.

An uncertain future

But many challenges lie ahead for the region. According to the report, noneconomic factors that could derail the region’s recent economic recovery include political uncertainty due to upcoming elections in several countries, geopolitical tensions, and extreme weather events.

Heightened economic risks externally—notably, a shift towards more protectionist policies and a sudden tightening of global financial conditions—could also weigh heavily on growth prospects.

Looking ahead, longer-term growth prospects for Latin America and the Caribbean remain subdued, suggesting that income levels in these countries are struggling to catch up to advanced economies.

The way forward

Despite recent gains in poverty and inequality reduction, Latin American and the Caribbean remain the most unequal region in the world. In response to these challenges and to secure durable growth that benefits all, policymakers in the region will need to implement key reforms and policies that focus on:

-

continuing to adjust to place debt ratios on a sustainable footing with a special attention to the quality of the adjustment;

-

further improving central bank communication and transparency to better deal with future shocks;

-

investing more in people through more efficient spending in education;

-

improving infrastructure, which would also boost other investment in the region;

-

tackling corruption by improving governance and the business climate;

-

opening up more to trade and financial markets, which can be seen as a step toward greater global integration; and

-

protecting gains from social spending.

Regional roundup*

Growth in South America is being led by the end of recessions in Argentina, Brazil, and Ecuador, higher commodity prices, and a moderation of inflation that has provided space for monetary easing.

In the near term, Mexico, Central America, and parts of the Caribbean are benefiting from stronger growth in the United States. Nevertheless, potential implications of the U.S. tax reform and ongoing renegotiations of the North American Free Trade Agreement (NAFTA) are also creating uncertainties for the region.

In Argentina, the current forecast is for real GDP growth of 2 percent in 2018. Even though high-frequency indicators suggest that economic activity remained robust in early 2018, the severe drought that hit the country will have a negative impact on agricultural production and exports. It is expected that next year the negative impact of the drought will be reversed.

In Brazil, real GDP is expected to grow at 2.3 percent in 2018, thanks to favorable external conditions and a rebound in private consumption and investment. The uptick in activity will lead to a moderate deterioration of the current account. A key risk, however, is that the policy agenda could change following the October presidential election, giving rise to market volatility and greater uncertainty about the medium-term outlook.

In Chile, economic activity is gaining momentum after a prolonged slowdown, benefiting from improved external conditions and domestic sentiment. Both mining and nonmining exports, as well as business investment, are leading the recovery, supported by solid household spending and slightly looser financial conditions.

In Colombia, policy easing and a favorable global environment will lift growth to 2.7 percent in 2018. A mildly expansionary fiscal policy, driven by stronger subnational government expenditure, along with the lagged effects of monetary policy easing in 2017, will support domestic demand. Investment is projected to increase strongly thanks to infrastructure projects, oil sector projects, and the 2016 tax reform.

Peru's government responded to the 2017 economic growth slowdown with countercyclical macro policies. These policies are expected to help economic growth rebound to around 3¾ percent in 2018, but downside risks associated with the Odebrecht investigation persist.

Venezuela's economic situation is worsening, with the economy contracting sharply for the fifth year in a row. The economy is expected to contract by 15 percent in 2018, following a cumulative 35 percent contraction over 2014–17. The humanitarian crisis is also intensifying with increasing scarcity of basic goods (for example, food, personal hygiene items, medicine), a collapse of the health system, and high crime rates. This has led to a sharp increase in emigration to neighboring countries.

The outlook for Central America, Panama, and the Dominican Republic (CAPDR) remains favorable and growth is expected to remain above potential for many countries in 2018, reflecting U.S. and global growth momentum.

Mexico's outlook is projected to benefit from higher growth in the United States as well as stronger domestic demand once uncertainty subsides about the outcome of the NAFTA renegotiation, the potential implications of the U.S. tax reform, and Mexico’s July presidential election. Output growth is expected to accelerate from 2 percent in 2017 to 2.3 percent in 2018, supported by net exports and remittances.

Prospects for the Caribbean region are improving, with growth in both tourism-dependent economies and commodity exporters projected to be in the 1–2 percent range for 2018 and 2019.