The world economy faces a sobering reality. The global growth rate—stripped of cyclical ups and downs—has slowed steadily since the 2008-09 global financial crisis. Without policy intervention and leveraging emerging technologies, the stronger growth rates of the past are unlikely to return.

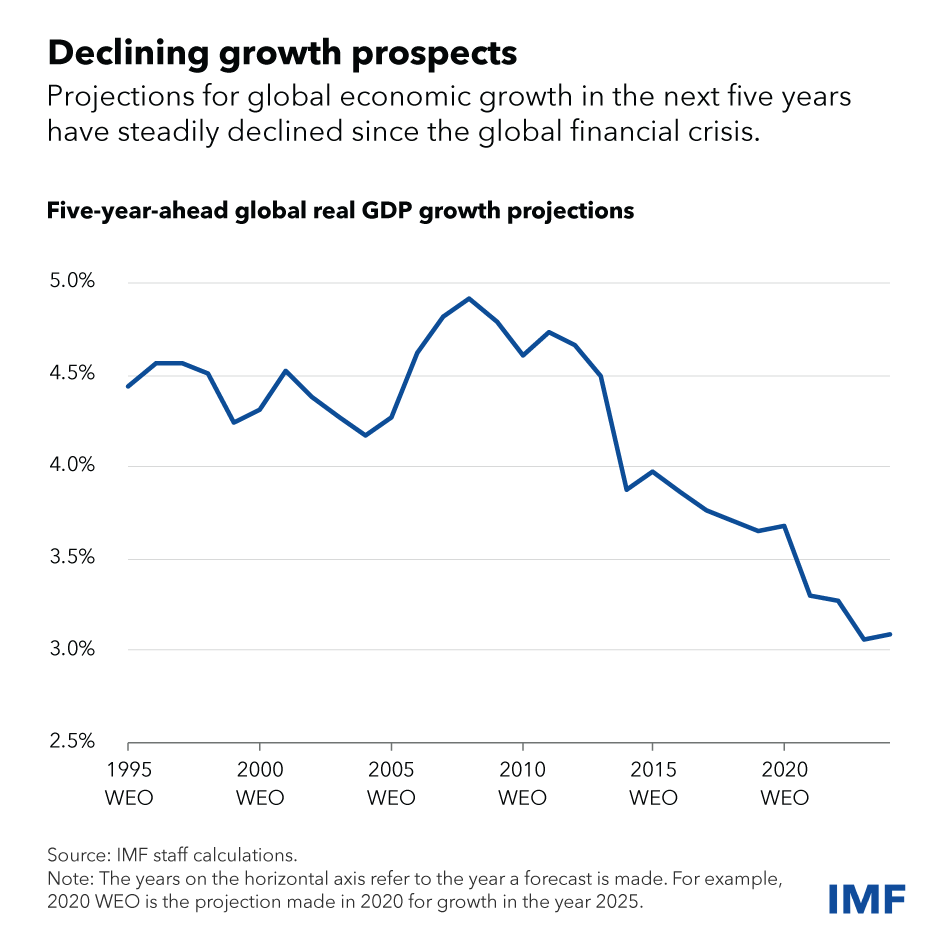

Faced with several headwinds, future growth prospects have also soured. Global growth will slow to just above 3 percent by 2029, according to five-year ahead projections in our latest World Economic Outlook. Our analysis shows that growth could drop by about a percentage point below the pre-pandemic (2000-19) average by the end of the decade. This threatens to reverse improvements to living standards, and the unevenness of the slowdown between richer and poorer nations could limit the prospects for global income convergence.

A persistent low-growth scenario, combined with high interest rates, could put debt sustainability at risk—restricting the government’s capacity to counter economic slowdowns and invest in social welfare or environmental initiatives. Moreover, expectations of weak growth could discourage investment in capital and technologies, possibly deepening the slowdown. All this is exacerbated by strong headwinds from geoeconomic fragmentation, and harmful unilateral trade and industrial policies.

However, our latest analysis shows that there’s hope. A variety of policies—from improving labor and capital allocation across firms to tackling labor shortages caused by aging populations in major economies—could collectively rekindle medium-term growth.

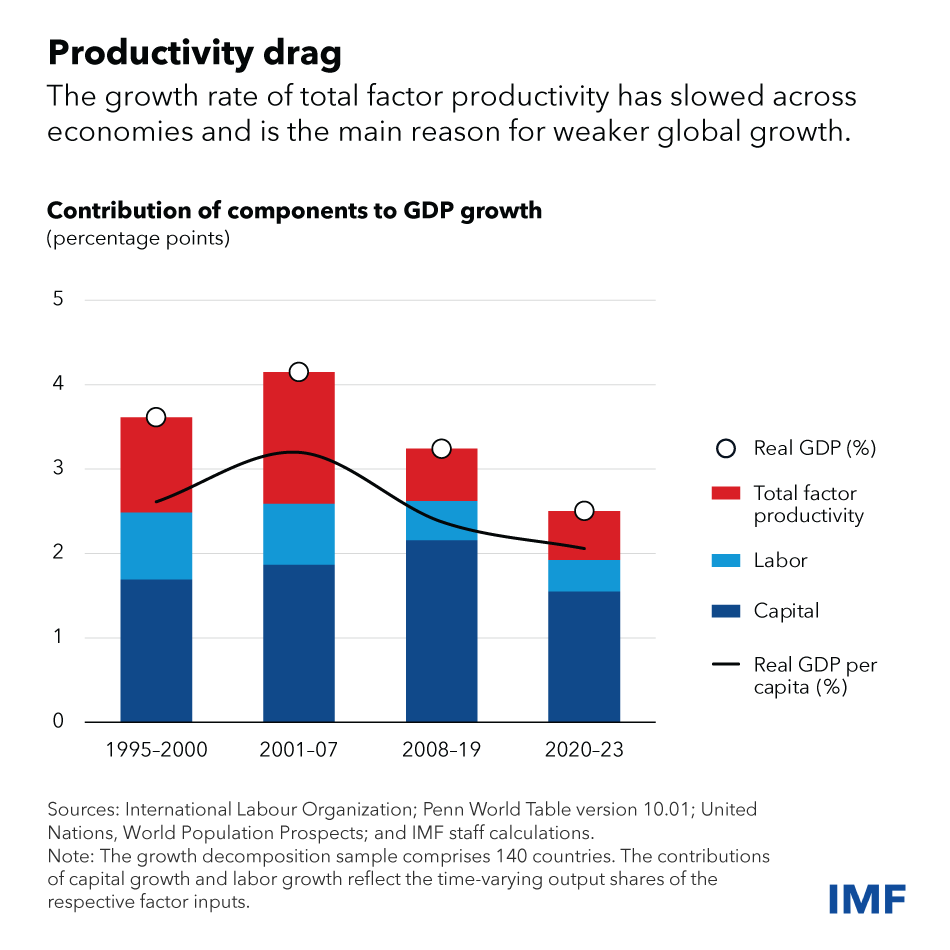

The key drivers of economic growth include labor, capital, and how efficiently these two resources are used, a concept known as total factor productivity. Between these three factors, more than half of the growth decline since the crisis was driven by a deceleration in TFP growth. TFP increases with technological advances and improved resource allocation, allowing labor and capital to move toward more productive firms.

Resource allocation is crucial for growth, our analysis shows. Yet, in recent years, increasingly inefficient distribution of resources across firms has dragged down TFP and, with it, global growth.

Much of this rising misallocation stems from persistent barriers, such as policies that favor or penalize some firms irrespective of their productivity, that prevent capital and labor from reaching the most productive companies. This limits their growth potential. If resource misallocation hadn’t worsened, TFP growth could have been 50 percent higher and the deceleration in growth would have been less severe.

Two additional factors have also slowed growth. Demographic pressures in major economies, where the proportion of working-age population is shrinking, have weighed on labor growth. Meanwhile, weak business investment has stunted capital formation.

Medium-term pressures

Demographic pressures are set to increase in most of the major economies, according to United Nations projections, causing an imbalance in world labor supply and dampening global growth. The working-age population will increase in low-income and some emerging economies, whereas China and most advanced economies (excluding the United States) will face a labor squeeze. By 2030, we expect the growth rate of the global labor supply to slide to just 0.3 percent—a fraction of its pre-pandemic average.

Some resource misallocation may correct itself over time, as labor and capital gravitate toward more productive firms. This will go some way toward mitigating the TFP slowdown even as structural and policy barriers continue to slow the process. Technological innovation may also lessen the slowdown.

But overall the pace of TFP growth is likely to continue to decline, driven by challenges such as the increasing difficulty of coming up with technological breakthroughs, stagnation in educational attainment, and a slower process by which less developed economies can catch up with their more developed peers.

Absent major technological advances or structural reforms, we expect global economic growth to reach 2.8 percent by 2030, well below the historical average of 3.8 percent.

Reviving global growth

Our analysis evaluates the impact of policies on labor supply and resource allocation, set against the backdrop of the rapid advance of artificial intelligence, public debt overhang, and geoeconomic fragmentation.

We examine scenarios featuring ambitious, but achievable, policy shifts that address resource misallocation by improving the flexibility of product and labor markets, trade openness, and financial development. We also consider policies aimed at enhancing labor supply or productivity by reforming retirement and unemployment benefits, supporting childcare, expanding re-training and re-skilling programs, and improving integration of migrant workers, as well as the removal of social and gender barriers.

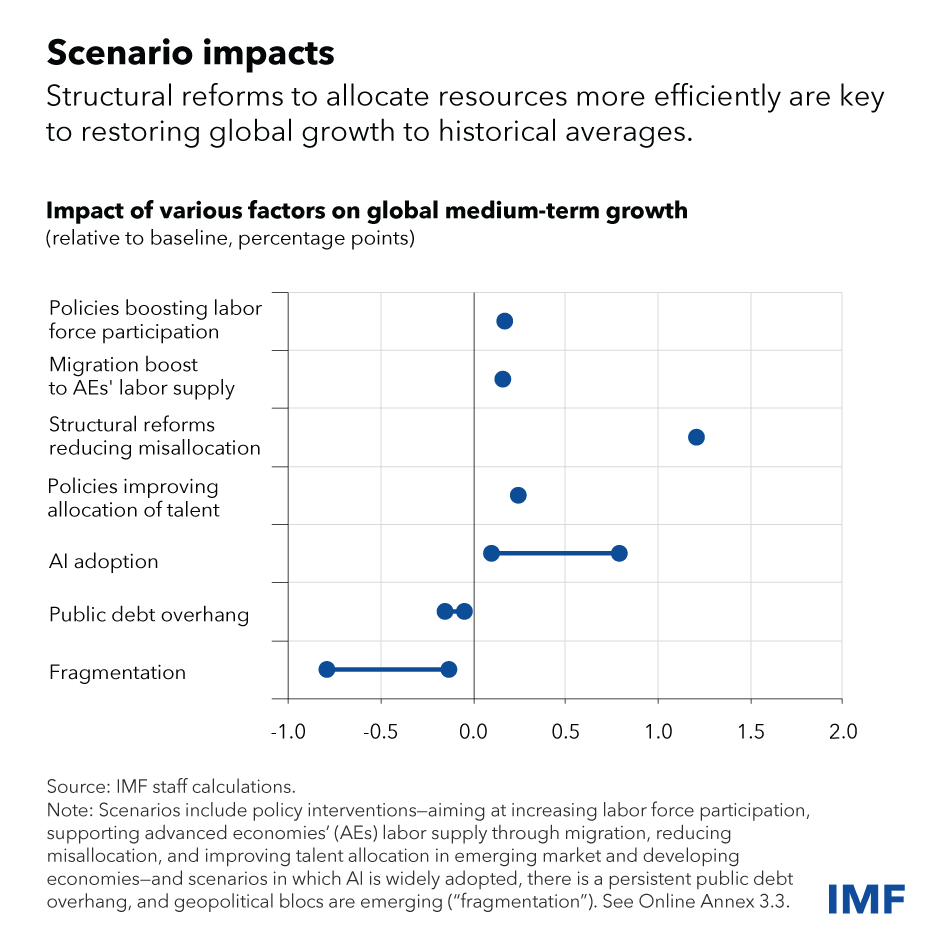

Our findings indicate that the benefits of increasing labor force participation, integrating more migrant workers into advanced economies, and optimizing talent allocation in emerging markets are comparatively modest.

By contrast, reforms that enhance productivity and fully leverage AI are key for reviving growth in the medium term. Our analysis suggests that focused policy actions to enhance market competition, trade openness, financial access, and labor market flexibility could lift global growth by about 1.2 percentage points by 2030. The potential of AI to boost labor productivity is uncertain but potentially substantial as well, possibly adding up to 0.8 percentage points to global growth, depending on its adoption and impact on the workforce.

In the long run, innovation-driven policies will be crucial to sustaining global growth.

—This blog, based on Chapter 3 of the World Economic Outlook, “Slowdown in Global Medium-Term Growth: What Will it Take to Turn the Tide?”, reflects research by Chiara Maggi, Cedric Okou, Alexandre B. Sollaci, and Robert Zymek.