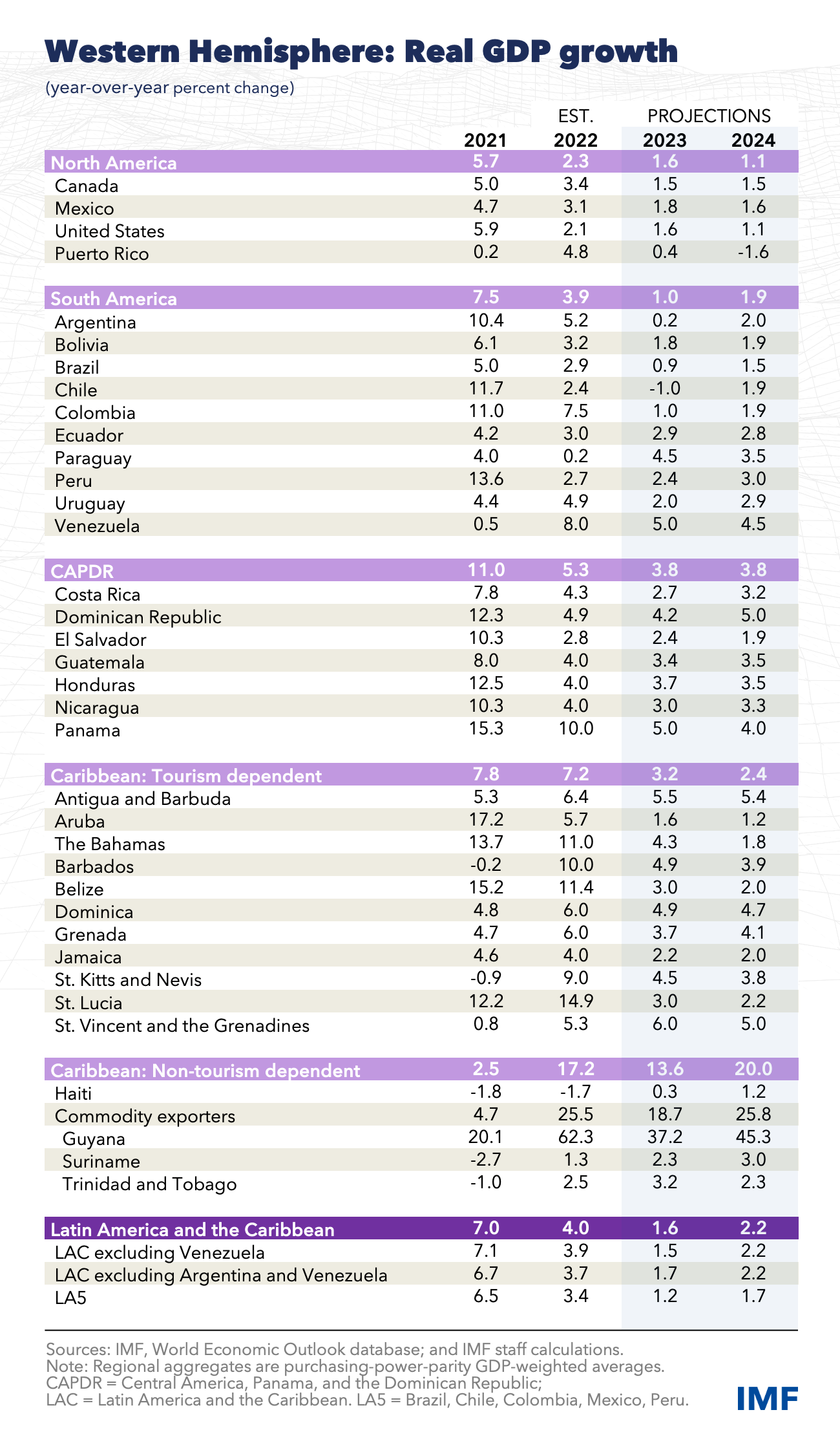

Growth in Latin America is projected to slow to 1.6 percent this year after a remarkable 4 percent in 2022. Price pressures that accompanied last year’s brisk economic activity appear to have peaked, but underlying inflation remains stubbornly high, disproportionally hurting low-income households who spend most of their earnings on food. To mitigate the risk that inflation becomes entrenched, fiscal policy can help monetary policy in reducing demand pressures.

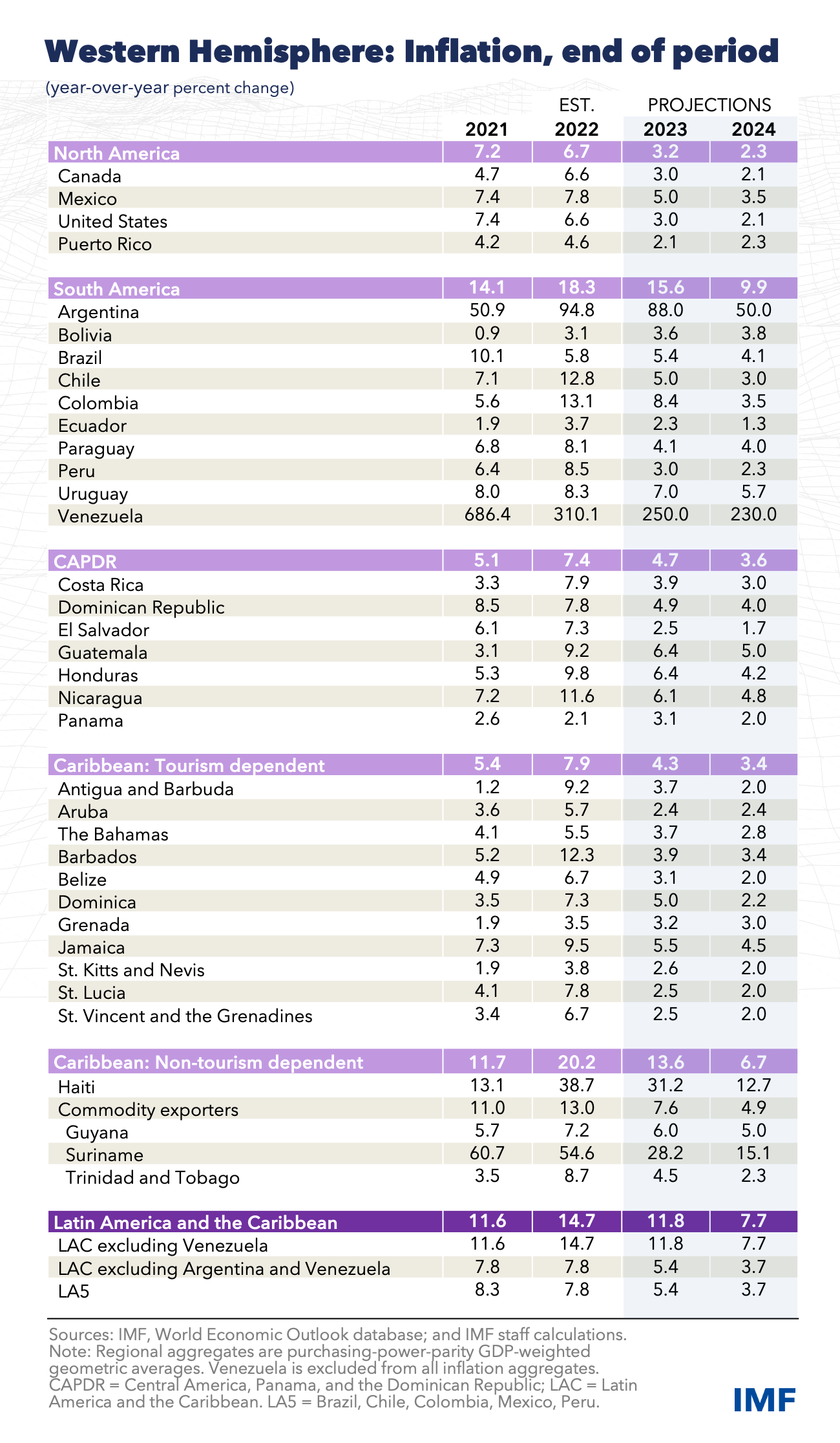

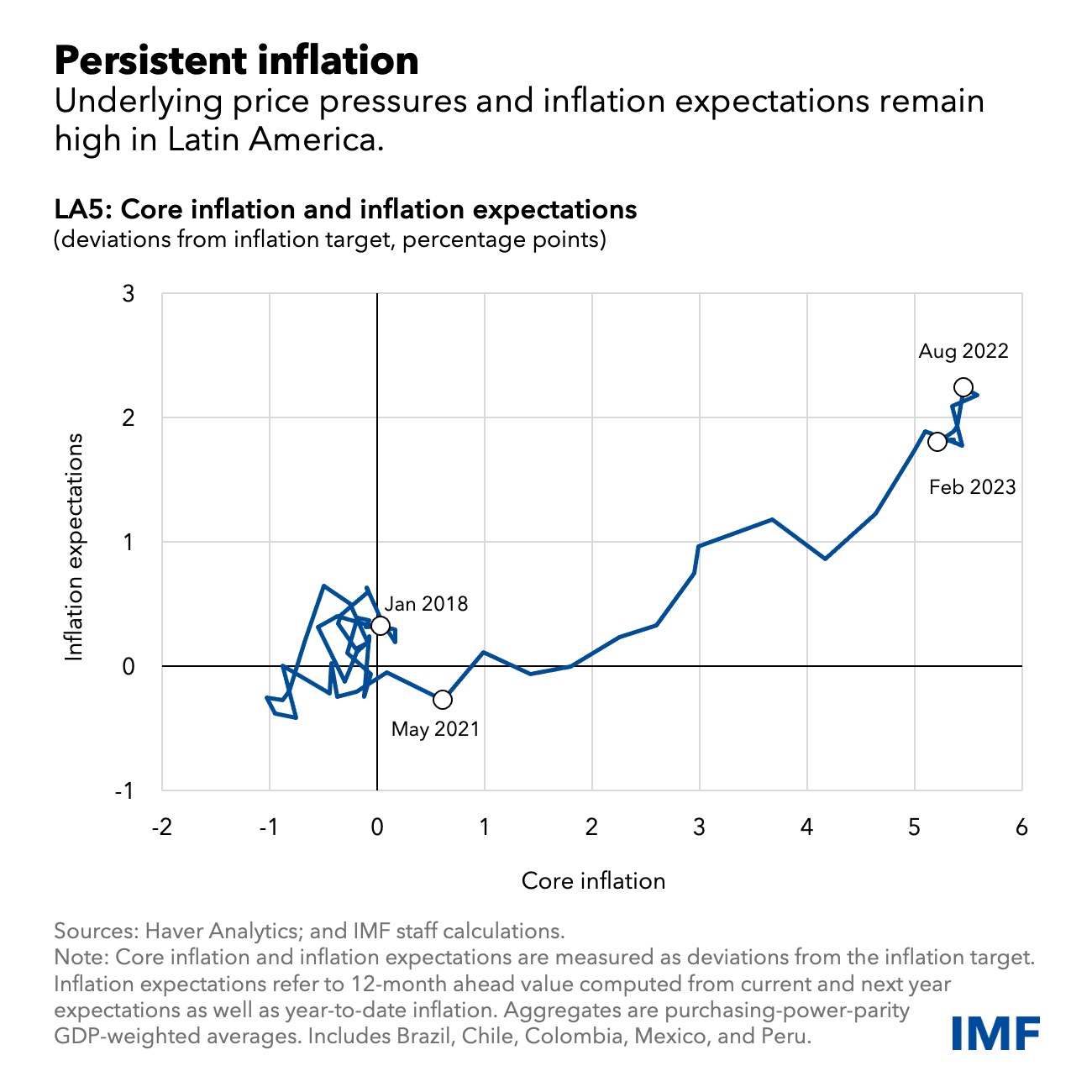

After peaking at 10 percent in mid-2022, headline inflation in the largest Latin American economies has slowed to 7 percent in March. However, this drop mostly reflects the fall of commodity prices from their peaks. Progress in bringing down core inflation, which excludes food and energy, appears to have stalled. Labor markets are tight, with employment firmly above its pre-pandemic levels. At the same time, output is at or above potential, and short-term inflation expectations exceed central banks’ target ranges. Strong domestic demand, rapid wage increases, and broad-based price pressures all point to a risk that inflation in the region could remain unacceptably high.

Tempering demand to tame price pressures

While most countries in the region have made important strides in price stability in the last two decades, the region’s history is full of examples of how high inflation can destabilize the economy and fuel inequality by hurting vulnerable groups most.

Restoring price stability is paramount to a healthy economy and protecting

the most vulnerable. In the current juncture, this requires slowing

domestic demand. With inflation—and especially core inflation—running

considerably above target and economies operating above potential,

policymakers no longer face the macroeconomic trade-off of 2021 and early

2022, when fighting inflation was at odds with the need to support the

recovery from the pandemic. Policies should be aimed at restraining demand

to bring it back into line with potential output. This will inevitably

require cooling the labor market.

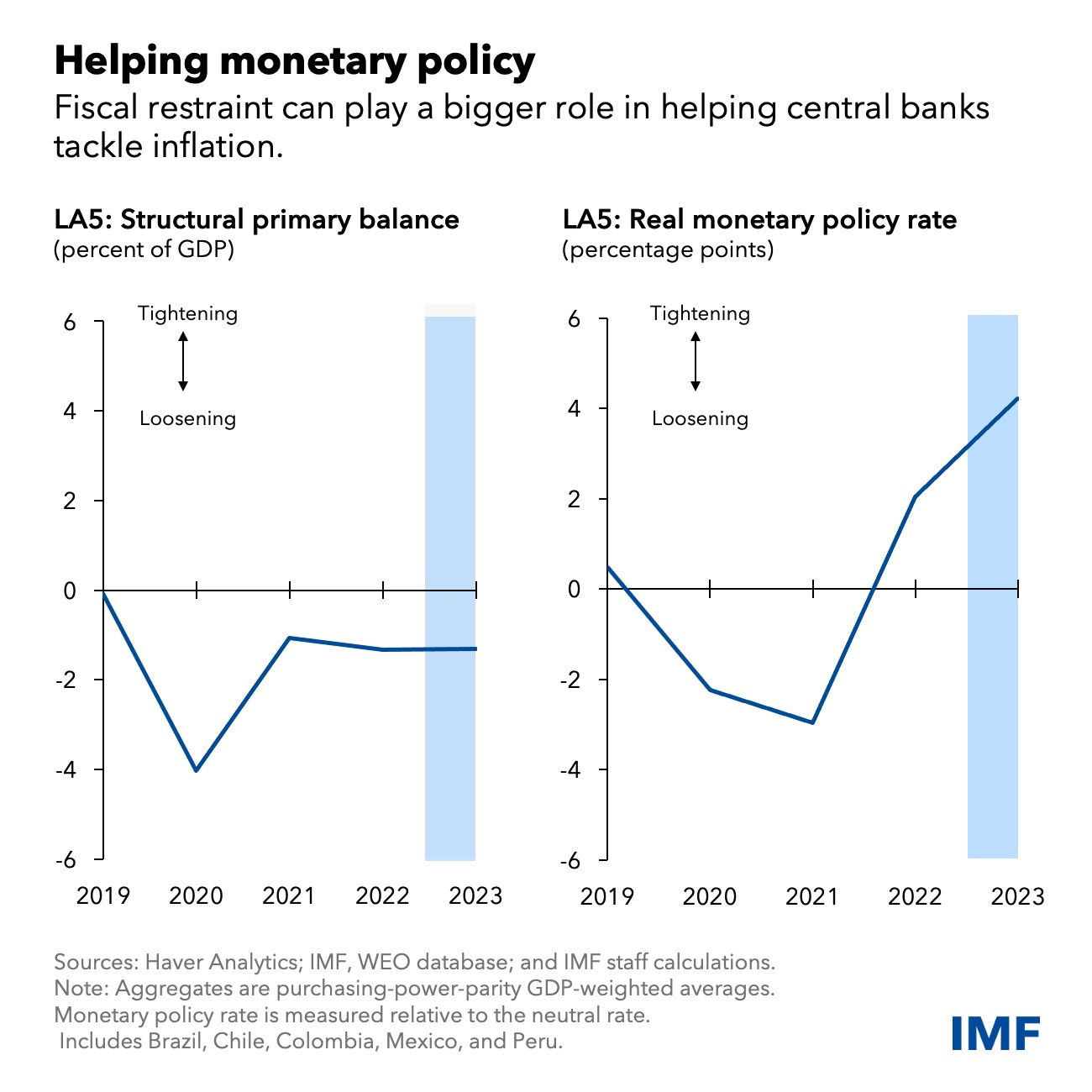

Decisive central bank rate increases have already done the heavy lifting. Furthermore, the recent financial stresses in some advanced economies could lead to tighter global financial conditions, which will further help cool demand. Given the usual lags between interest rate increases and their effect on economic activity, the full impact of the tightening that has already been undertaken should be seen most clearly during the course of this year, contributing to slower growth this year.

However, with inflationary pressures proving persistent, central banks will need to remain resolute in their fight until there is an unambiguous downward path for prices. Interest rates will likely need to remain high for much of this year and, in some cases, even into next year. This will guide inflation back to target by late 2024 or early 2025.

A more balanced policy mix

To assist central banks in their battle against inflation, fiscal policy could play a bigger role through a more countercyclical stance this year. As recent IMF research shows, fiscal tightening makes it possible for central banks to increase rates by less to bring down inflation.

The fiscal stimulus of 2020, which was essential to support economies

during the pandemic, has been mostly withdrawn, but fiscal policy this year

is expected to be broadly neutral in most countries. A more contractionary

fiscal stance would help slow domestic demand, allowing interest rates to

start coming down sooner. This would reduce potential financial stability

risks from keeping interest rates higher for longer and help to bring down

public debt levels, creating more policy space to respond to the next

economic shock. That is, a more balanced policy mix would improve the

prospects of taming inflation and reducing the risks of a recession.

Rebalancing policy will not be easy. Demands for social spending in the region are high. There are serious distributional and social equity issues to contend with. Enacting tax policies that require the wealthy to pay their fair share should be part of the solution.

But policymakers will also need to find savings without cutting into key social programs or spending on health, education, and public infrastructure. There is important scope to reduce inefficiencies in public spending, and people are more likely to embrace more prudent public finances if services are provided with greater efficiency. Being good stewards of taxpayer resources could also help reverse the erosion of trust in government that many countries have suffered over the last several years.

This agenda is challenging, but restoring price stability is paramount to protecting the poor and durably addressing social demands. Relying more on fiscal policy in taming inflation makes sense from a macroeconomic perspective and, if policies are well-designed, can be achieved in a socially equitably way.