Increased R&D spending isn’t necessarily boosting US productivity as industrial giants focus on defending their turf

Investing more in research and development, we’ve long assumed, is a surefire way to spur innovation, increase productivity, and fuel job creation and economic growth. And yet, as the US dramatically expanded R&D spending over the past four decades, the opposite happened. Innovation, productivity gains, and economic expansion slowed. What went wrong?

Real-world data show that there’s more nuance to encouraging innovation than simply throwing money at it. Giant enterprises came to dominate vast swaths of the American economy, crowding out more innovative smaller businesses and start-ups. Across sectors, the biggest players prioritized strategic moves to defend their businesses rather than seeking genuine innovation, and as a result the economy missed potential growth opportunities, according to recent research.

Such findings suggest it’s time to rethink and better focus the American approach to ensuring innovation and economic growth. Policymakers need to encourage not only R&D but also the more effective allocation of resources. A look at how US innovation changed over the past few decades suggests how they can do that.

Double-edged sword

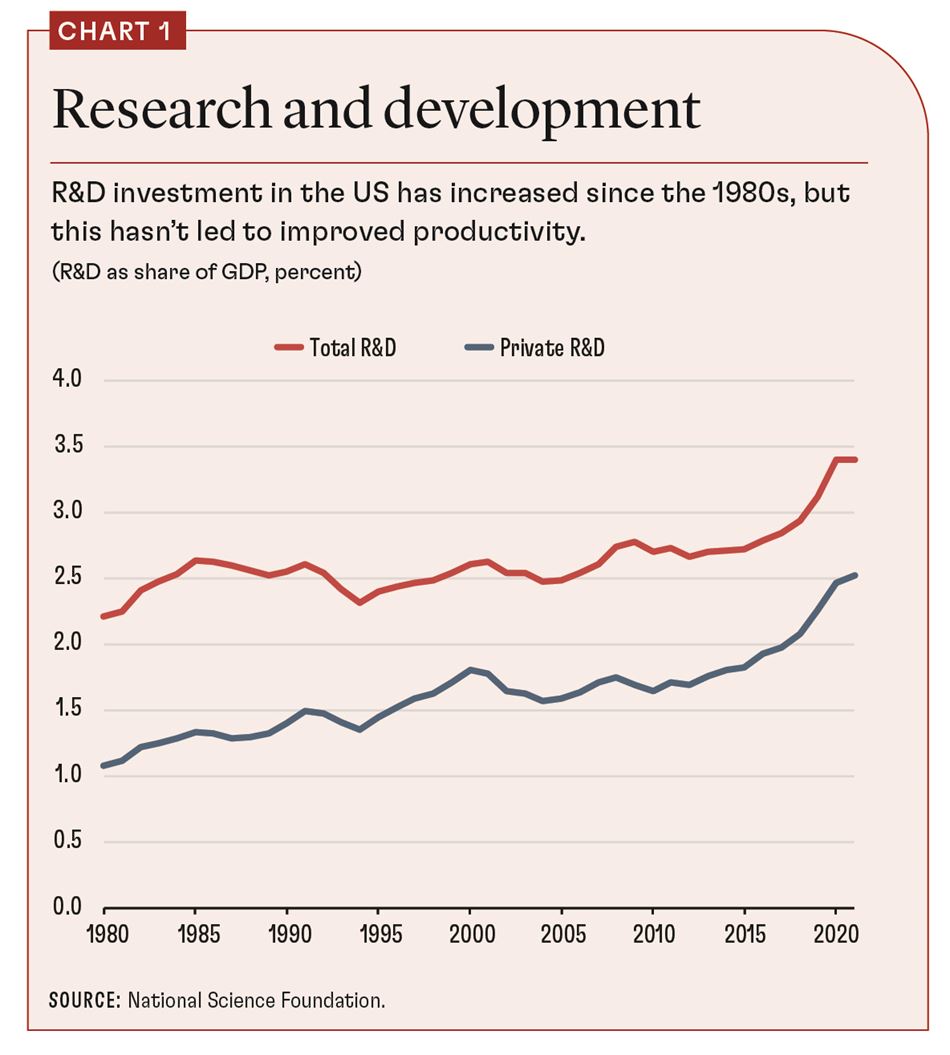

In the 1980s, total US R&D investment represented 2.2 percent of GDP. Today, that figure is 3.4 percent, according to the National Science Foundation (see Chart 1). Private R&D spending by businesses more than doubled, to 2.5 percent of GDP from 1.1 percent.

Based on conventional economic models, that kind of increase in R&D spending should have led to accelerated economic growth rather than the slowdown that actually occurred. Productivity growth between 1960 and 1985 averaged 1.3 percent. Over the subsequent three and a half decades, gains in productivity fell below that average, except for a brief uptick in the early 2000s, and annual growth has generally been declining.

To understand how conventional analysis so badly missed the mark, we need to move away from aggregate data and examine the structure and distribution of R&D spending in the US using high-quality microdata on businesses, inventors, and innovations.

The Census Bureau’s Nathan Goldschlag and I conducted extensive studies to understand the factors behind the productivity paradox. We found a significant shift in the US landscape of innovation. Over the past two decades, the proportion of the population involved in patent production nearly doubled, while productivity growth fell by half.

The explanation may lie in how R&D spending is allocated. In earlier research, Harvard’s William Kerr and I found that small businesses are more innovative relative to their size, suggesting they use R&D resources more efficiently. As companies grow and dominate their markets, they often shift their focus from innovation to protecting their market position.

In a more recent study, Salome Baslandze, Francesca Lotti, and I showed using Italian data that larger enterprises tend to innovate less and instead engage in activities that limit competition. One such activity is hiring local politicians. As businesses climb the ranks among the largest 20 players in their industry, they hire more politicians, while their patent production declines. This highlights what we call a leadership paradox, where leading companies plow resources into maintaining dominance rather than fostering innovation.

This shift in focus among big businesses might be a pivotal factor in the US productivity slowdown. As dominant players prioritize strategic moves over genuine innovation, the economy as a whole is almost certainly missing out on potential growth opportunities. Understanding this dynamic is crucial for policymakers seeking to effectively encourage true innovation and drive economic growth.

Over the past two decades, there has been a notable reallocation of innovative resources toward large, established companies, Goldschlag and I documented in 2022. At the beginning of this century, roughly 48 percent of American inventors worked for these big incumbent companies—those that are more than 20 years old and employ more than 1,000 workers. By 2015, that figure had surged to 58 percent, marking a significant shift in where the nation’s innovative talent is concentrated.

At first glance, this shift might not seem problematic. After all, the big companies might have the resources to support extensive R&D. However, research shows a concerning trend: inventors that move to large firms become less innovative compared with inventors that move to young firms.

Innovation-stifling hiring

A specific practice identified in our research is innovation-stifling hiring. This occurs when big, established enterprises hire key employees from younger competitors, often by offering higher salaries. However, instead of using these new employees to drive innovation, the big businesses may place them in roles that do not fully leverage their skills. As a result, these individuals become less innovative, and the overall innovative capacity of the economy suffers.

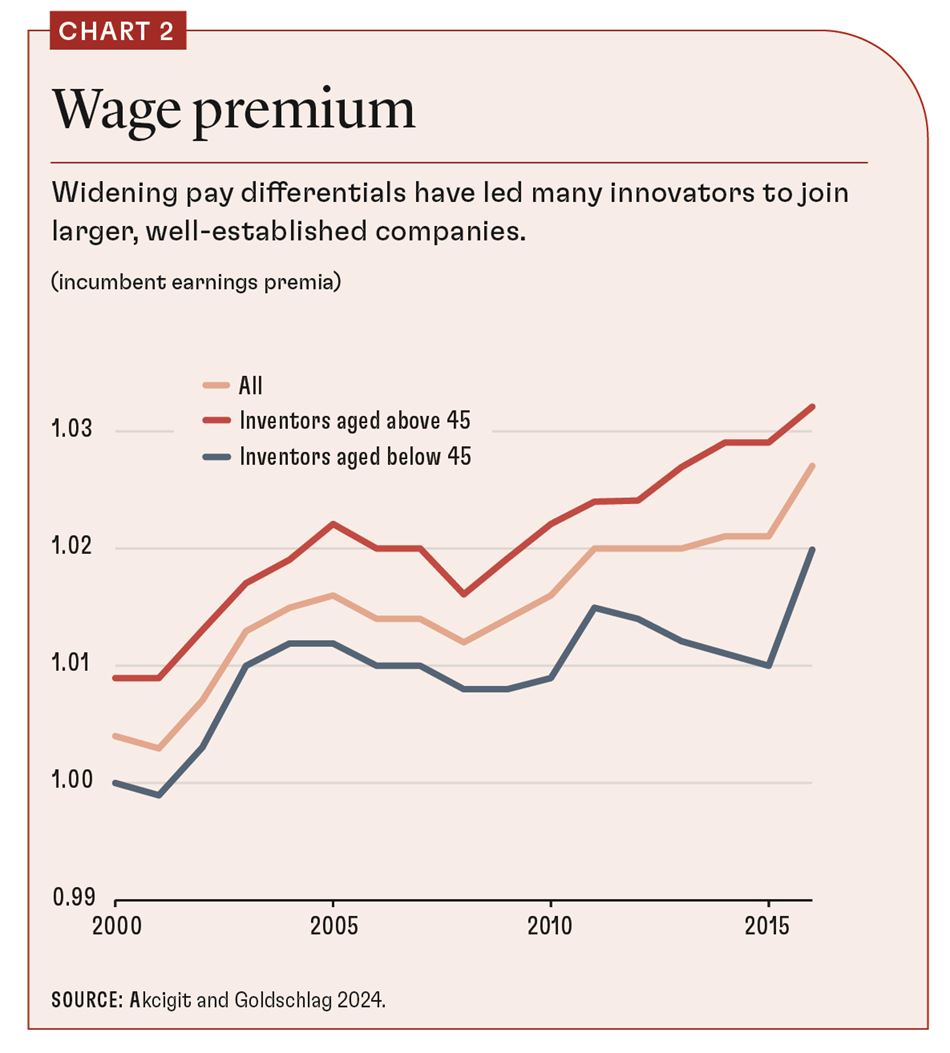

After 2000, there was a notable increase in the wage premium offered by established companies, compared with salaries paid by younger businesses. The pay differential widened by 20 percent, prompting many innovators to switch jobs and join larger, well-established companies (see Chart 2). However, these inventors’ innovativeness dropped by 6 percent compared with that of their peers who joined younger employers.

One interpretation of this practice could be that it serves as a strategic move by large enterprises to neutralize potential competitive threats. By hiring away top talent from rivals, these companies not only weaken their competitors but also prevent these individuals from contributing to potentially disruptive innovations elsewhere. This strategy may benefit the hiring business in the short term, but it poses a long-term risk to the economy’s overall innovation and growth.

This suggests that while the US has been increasing overall R&D spending relative to GDP, the shift of inventive talent toward large, old businesses has not led to the expected boost in productivity. These industrial incumbents often prioritize maintaining their market dominance over pushing the boundaries of innovation. This defensive stance means that even though more resources are being funneled into R&D, they are not being used as effectively as they could be in smaller, more agile companies.

Consequently, the US economy is not benefiting from growth in productivity spurred by R&D spending. This underscores the importance of not just the amount of R&D investment but also where and how it is allocated. To truly harness the power of innovation, policies and incentives need to shift to encourage more dynamic, risk-taking behavior, particularly among smaller enterprises and start-ups. This could lead to the kind of productivity gains the US needs.

Perverse incentives

The debate around the role of industrial policy in the US has intensified, with a renewed emphasis on strong industrial strategies. Reflecting on past experiences can offer valuable insights. The Federal Reserve’s Sina Ates and I examined market competition trends in the US over the past several decades. Since the early 1980s, there’s been a noticeable increase in market concentration and a decline in business dynamism, we found.

This period aligns with the 1981 introduction of the R&D tax credit, a component of President Ronald Reagan’s sweeping Economic Recovery Tax Act. The credit was intended to encourage businesses to invest in research and development. Minnesota was the first state to adopt a similar state-level R&D tax credit, in 1982, and many other states followed, expecting to promote innovation and economic growth.

Which companies are most likely to take advantage of the R&D tax credit? Our research with Goldschlag shows that large businesses are much more likely to benefit than smaller ones. The policy—perhaps unintentionally—favors big companies, encouraging them to dominate in R&D spending.

When we combine this observation with the innovation-stifling hiring practices of large businesses, a pattern emerges. Can policy be linked to more of these practices? It seems the answer is yes. Our research provides direct evidence that businesses actively claiming R&D tax credits are more likely to engage in such practices. These enterprises often offer higher salaries to inventors, and the inventors become less innovative after joining. This suggests that innovation subsidies, while intended to encourage research and development, might inadvertently reduce overall innovation by creating different incentives for market leaders compared with smaller, younger rivals.

The evidence suggests that while the US is investing more in R&D, the concentration of resources among large businesses has led to diminishing returns in terms of productivity growth. This outcome challenges the assumption that simply expanding R&D spending will automatically lead to economic growth. Instead, it highlights the need for a more nuanced approach to industrial policy—one that not only incentivizes R&D but also encourages the effective reallocation of resources.

To foster a more dynamic and innovative economy, the US needs to design policies that support not just large incumbents but also smaller businesses and start-ups, which often have a greater capacity for disruptive innovation. This could include targeted tax credits for small businesses, grants for early-stage innovation, and policies that encourage competition and reduce barriers to entry for new players.

While the US has significantly increased R&D spending over a sustained period, the benefits haven’t been evenly distributed, contributing to the slowdown in productivity growth. Policymakers need to reconsider the use of traditional industrial policies, which may have led to reduced competition and slower productivity gains. It’s not just about the total amount spent on R&D but also how it’s allocated. By creating a more inclusive innovation ecosystem, the US can better tap its innovative talent, boosting economic growth and securing future prosperity.

UFUK AKCIGIT is the Arnold C. Harberger Professor of Economics at the University of Chicago, a research associate with the National Bureau of Economic Research, and a research affiliate at the Centre for Economic Policy Research.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.

References:

Akcigit, Ufuk, and Sina Ates. 2021 “Ten Facts on Declining Business Dynamism and Lessons from Endogenous Growth Theory.” American Economic Journal: Macroeconomics 13 (1): 257–98.

Akcigit, Ufuk, Salome Baslandze, and Francesca Lotti. 2023. “Connecting to Power: Political Connections, Innovation, and Firm Dynamics.” Econometrica 91 (2): 529–64.

Akcigit, Ufuk, and Nathan Goldschlag. 2022. “Where Have All the ‘Creative Talents’ Gone? Employment Dynamics of US Inventors.” NBER Working Paper 31085, National Bureau of Economic Research, Cambridge, MA.

Akcigit, Ufuk, and Nathan Goldschlag. 2024. “Understanding the Innovation Puzzle: Firm Size, Inventors, and Industrial Policy.” University of Chicago Working Paper, Chicago, IL.

Akcigit, Ufuk, and William Kerr. 2018. “Growth through Heterogeneous Innovations.” Journal of Political Economy 126 (4): 1374–443.

The Census Bureau has ensured appropriate use of confidential data and reviewed for compliance with disclosure-avoidance rules (Project 7083300: CBDRB-FY24-CES007-01).