Opening Remarks at the Press Conference for the Regional Economic Outlook for Europe

April 24, 2025

Welcome to today’s press conference on the economic outlook for Europe.

Since our last briefing in October, the global economy has seen fundamental shifts in trade policies.

Forecast

We have downgraded Europe’s growth outlook as a result.

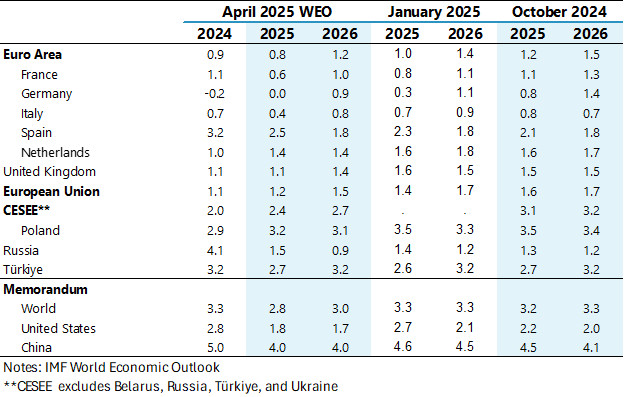

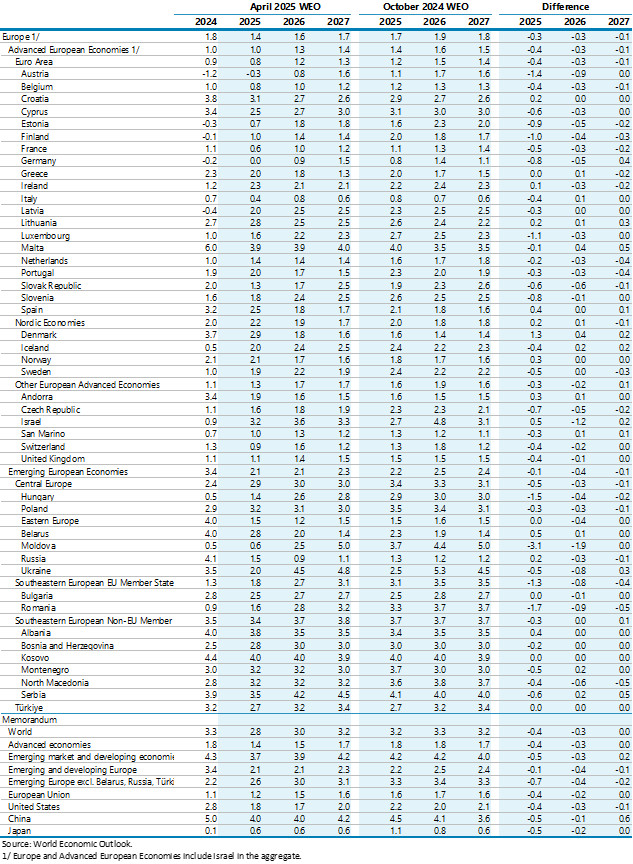

- For the euro area, we forecast growth rates of 0.8 and 1.2 percent for 2025 and 2026. The size of the downgrade relative to our latest forecast in January 2025 is -0.2 percentage points for both years and broad based across countries (Table 1).

- The increase in US tariffs[1], elevated uncertainty and tighter financial conditions are weakening activity in 2025 and weigh on the expected pick up in domestic demand in 2026 and 2027.

Table 1 World Economic Outlook, Growth Forecast, Selected Countries.

(Percent; Annual Growth)

- Risks to growth are to the downside as trade tensions and uncertainty could deteriorate further. Financial conditions could become tighter, and even though the financial system generally appears resilient, strains could occur. Larger fiscal easing due to higher defense spending and lower energy prices are upside risks, especially beyond 2025.

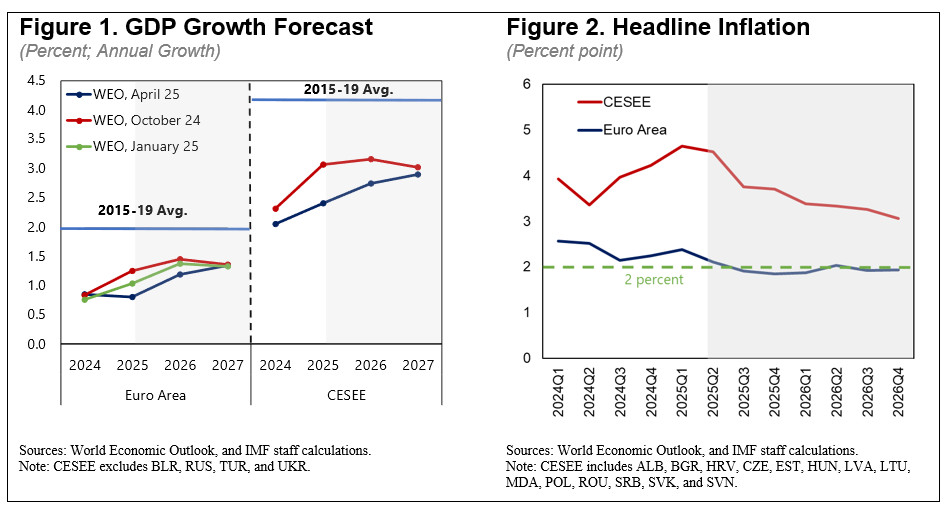

- Growth in the Central, Eastern, and Southeastern European (CESEE) region[2] has been downgraded by more. Our forecast is for 2.6 and 3.0 percent growth in 2025 and 2026 (Figure 1). This sizeable downgrade is primarily due to a comparatively larger trade-exposed manufacturing sector in the region.

The downgrades would have been larger if there were not offsetting factors.

- New public spending such as Germany's €500 billion infrastructure package and increased defense spending across Europe are supporting demand going forward. Overall, the impacts of this extra spending on euro area growth are 0.1 and 0.2 percentage points of GDP in 2025 and 2026.

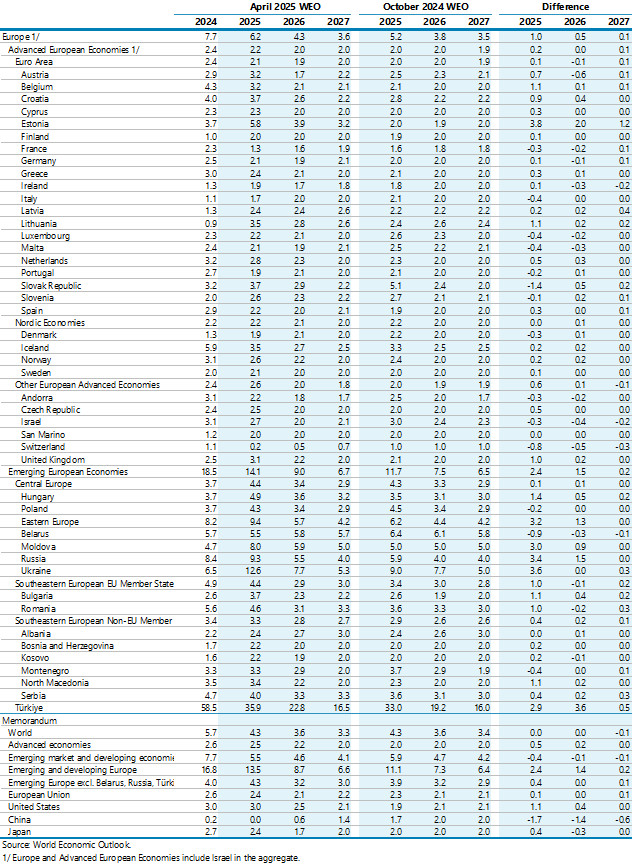

On the inflation front, we see faster convergence to targets driven by lower energy prices and dampened demand (Figure 2).

- Euro area inflation is forecast to reach target sustainably in the second half of 2025 slightly faster than previously anticipated due to lower energy prices and softer demand.

- However, for the CESEE region, inflation rates are likely to remain above targets well into 2026 and for some until 2027 due to persistent services inflation and high labor costs. In several countries, such as Romania, Hungary, and Poland, high wage growth may take time to come down and could slow disinflation.

Medium-Term Outlook

Europe’s medium growth prospects need some bolstering. The changes in the external environment come at a time of deep structural transformations:

- Europe’s population is aging, and by 2050 the working-age population will have shrunk in more than two-thirds of EU countries.

- The arrival of new technologies in automobile and AI sectors have the potential to transform entire industries and services, and

- energy costs have risen sharply.

- Finally, private investment and productivity growth have slowed for some time. As we have shown in recent work (IMF October 2024), European firms have fallen behind the global productivity frontier.

What is missing? Our research points to Europe’s still very fragmented single market (IMF October 2024a).

- This includes barriers in goods and services markets and segmented capital and labor markets which limit companies’ incentives and ability to innovate and scale up (Arnold, Claveres and Frie, 2024).

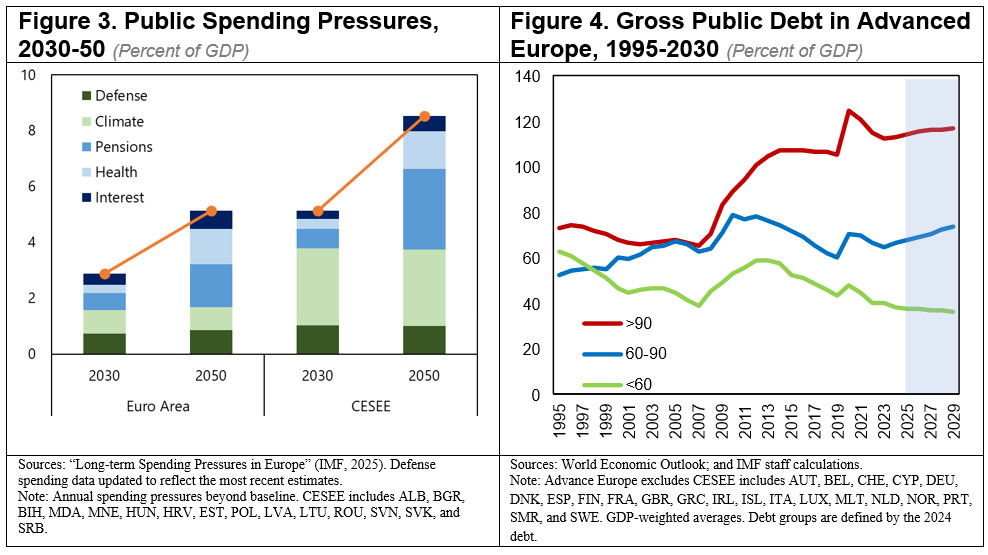

- Over the next 25 years, social, defense, and climate spending alone will add almost 5 ¾ percentage points of GDP to budgets in advanced economies, and 8 percentage points in emerging Europe (Eble et al., 2025).

Policy Prescriptions

So, what type of policies should Europe implement to navigate these turbulent times and secure the future?

First, Europe should aim for more, not less trade.

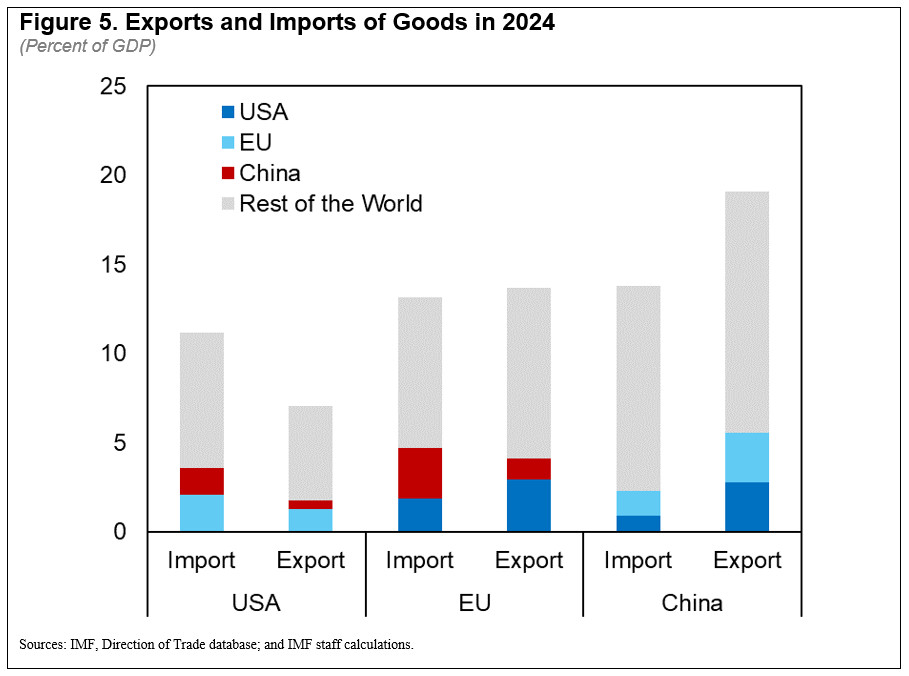

- Preserving openness is crucial given the importance of trade (Figure 5), and Europe should continue to expand its network of free trade agreements.

- When dealing with trade shocks, any support to viable businesses aimed at mitigating tariff impacts should be temporary and targeted. Europe should protect people, but we have to be cautious not to stand in the way of inevitable structural change.

- Lastly, the impact of possible trade diversion should be carefully assessed. Large tariffs between the U.S. and China will potentially bring additional imports into Europe. Our preliminary estimates are for higher imports from China of around 0.25 percent of EU GDP in the near term. Trade diversion would likely also lower input costs for European firms and prices for consumers. Overall, impacts from this channel would appear to be of a manageable magnitude. And European exports will likely be affected as well.

- The net effects of all this are difficult gauge. This makes it even more important that sector-specific safeguards should only be considered where viable firms are at risk. Measures should align with WTO principles, be time-limited, and well-communicated.

Second, European policy makers should ensure stability through balanced macroeconomic policies.

- Inflation rates are now close to targets. With the tremendous success of the ECB’s disinflation effort, central banks should continue to normalize monetary policy with caution. Global tensions could cause inflation expectations to drift up again, though a deeper economic downturn in Europe would pressure them downward.

- Monetary policy must remain agile and focused on durably reaching targets. We recommend that the ECB lower the policy rate to 2 percent this summer and maintain it there, barring major shocks. In CESEE countries, where inflation is still higher and more persistent, central banks should ease cautiously.

- For most countries, rebuilding fiscal buffers remains a priority. Those with low deficits and debt can temporarily accommodate priority defense spending, but they will need to return to debt sustainability goals over time. Countries with high debt levels should either reallocate spending or boost fiscal revenues without delay.

Finally, Europe must meet the moment and focus on growth and resilience. Embracing its structural reform agenda at the EU and national level can unlock Europe’s growth potential and make it more robust.

- Barriers to trade within the EU are still substantial (Adilbish et al., 2025).

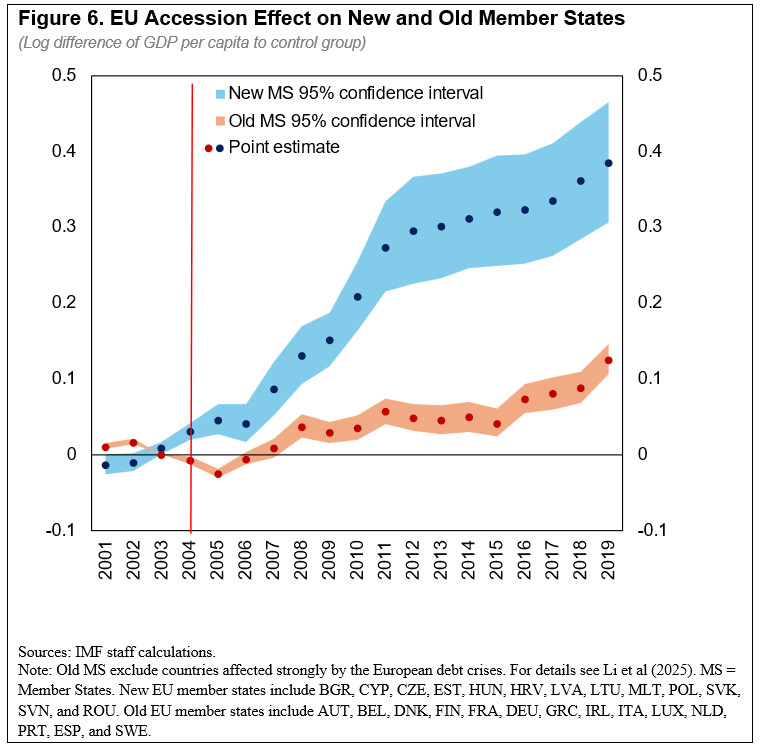

- The potential power of integration is immense (Figure 6) The last enlargement wave in 2004, led new member states to increase their GDP per person by 30 percent after 15 years versus what it would have been without accession (IMF October 2024b).

- In forthcoming work, we estimate that selected, actionable EU-level reforms could increase EU GDP by around 3 percent over the next decade. Key areas for improvement include lowering barriers to labor mobility, enhancing the functioning of capital markets, creating a more integrated electricity market, and harmonizing laws and regulations, such as through a 28th regime (IMF, 2025). These reforms would also make Europe’ economy more resilient to shocks.

- But there is also large untapped growth potential on the domestic front. In another forthcoming study, we find that comprehensive national reforms could raise real GDP levels by about 5 percent in advanced Europe and between 7 to 9 percent in the CESEE region. These reforms would remove inefficiencies at home and complement EU-wide reforms. The biggest gains would come from raising skills of workers and improving the functioning of labor markets. For most advanced European economies, national reforms should also focus on boosting innovation. For several CESEE countries large gains would come from strengthening the rule of law and combatting corruption.

Successful implementation of these reforms will require political will. The potential gains are large. Progress is now urgently needed for Europe to grow and maintain its quality of life.

Thank you.

References

Adilbish, O. Cerdeiro, D., Duval, R., Hong, G.H., Mazzone, L., Rotunno, L., Toprak, H., and Vaziri, M., 2025, “Europe's Productivity Weakness”, IMF Working Paper No. 2025/040,

Arnold, N., Claveres, G. and Frie, J.M., 2024, “Stepping up venture capital to finance innovation in Europe”, IMF Working Paper No. 2024/146

Eble. S., Pitt. A., Bunda, I., Adilbish, O.E., Budina, N., Hong, G.H., Malak, M.T., Mohona, S., Myrvoda, A. and Primus, K.,2025, "Long-Term Spending Pressures in Europe", IMF Departmental Papers 2025

IMF October 2024 Regional Economic Outlook: Europe 2024 A Recovery Short of Europe’s Full Potential.

IMF October 2024 Regional Economic Outlook: Europe, 2024a, Europe’s Declining Productivity Growth: Diagnoses and Remedies Note 1

IMF October 2024 Regional Economic Outlook: Europe, 2024b, Accelerating Europe’s Income Convergence through Integration Note 2

IMF, 2025. “Staff Background Note on EU Energy Market Integration” for EFC, January 2025.

Annex Table 1.1 Real GDP Growth

(Year-over-year percent change; aggregation based on GDP in purchasing power parity terms)

Annex Table 1.2 Headline Inflation

(Year-over-year percent change; aggregation based on GDP in purchasing power parity terms)

[1] The forecast includes all tariff announcements (US tariffs on the EU) up until April 4, 2025, at an estimated US effective rate of about 15 percent.

[2] Excluding Belarus, Russia, Türkiye and Ukraine.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER:

Phone: +1 202 623-7100Email: MEDIA@IMF.org