Businessman takes a phone call in Singapore. Asia is caught in a period of global policy uncertainty (photo: rawpixel/istock)

Prolonged Uncertainty Weighs on Asia's Economy

October 22, 2019

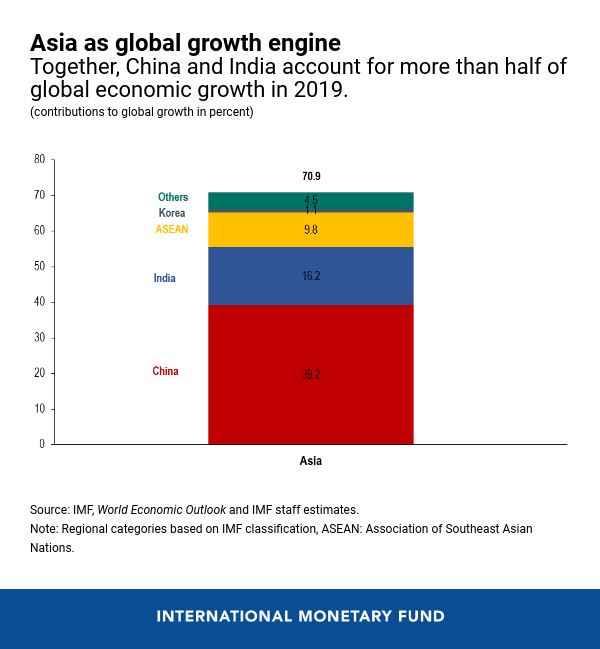

Asia’s strong trade and financial integration is a manifestation of the region’s success. However, this can also be a source of vulnerability amid continuing weakness in global trade and investment, and the region is caught in prolonged global policy uncertainty. Nonetheless, Asia remains the fastest-growing region in the world, accounting for more than two-thirds of global growth in 2019.

The near-term outlook points to continued slowdown of regional growth, driven by global policy uncertainty and slowing growth in China and India. With Asia’s conjuncture at a delicate moment, policies will need to be supportive while safeguarding financial stability.

- Chang Yong Rhee, Director of the IMF’s Asia and Pacific Department

Related Links

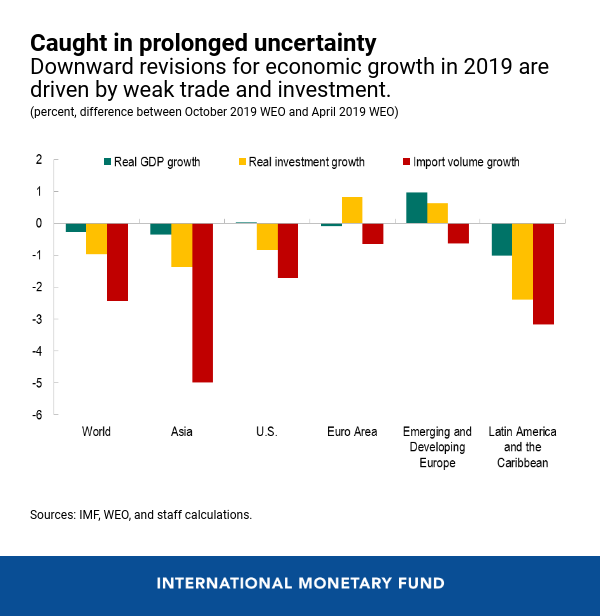

The IMF’s latest economic assessment for Asia and the Pacific highlights rising downside risks to growth in the context of a synchronized global slowdown. Growth in Asia softened in the first half of 2019, driven by a pronounced decline in fixed investment and exports. Consumption largely held up, helped by supportive policies across the region.

Downward growth revisions

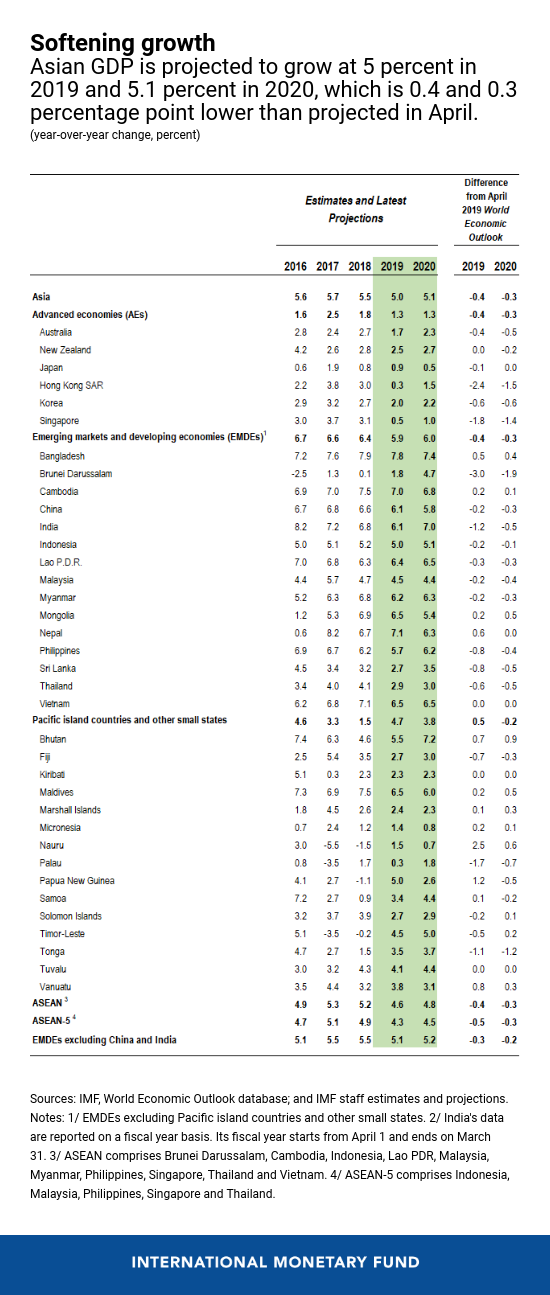

The report finds that Asia is projected to grow at 5 percent in 2019 and 5.1 percent in 2020—0.4 and 0.3 percentage point lower than projected in April. This would constitute the slowest pace of expansion since the global financial crisis. Downward revisions for growth in Asia are larger than for the global average and particularly pronounced in investment and trade. Nonetheless, Asia still remains the fastest-growing major region in the world, accounting for more than two-thirds of global growth in 2019. China alone accounts for 39 percent of global growth, India 16 percent, and ASEAN 10 percent.

China’s growth is expected to moderate to 6.1 percent in 2019, and 5.8 percent in 2020. The gradual deceleration reflects the ongoing rebalancing of growth drivers, and the adoption of new trade measures by the United States and China since May, which will be partly offset by policy stimulus.

In India, growth decelerated sharply in recent quarters but is set to strengthen from 6.1 percent in fiscal year 2019 to 7 percent in 2020, supported by recent monetary policy stimulus and the announced corporate income tax reduction.

After a period of robust growth, Japan’s economy is projected to expand at a moderate pace in line with potential growth (0.9 percent in 2019 and 0.5 percent in 2020). The drag on private consumption from the recent consumption tax hike is expected to be mitigated by temporary fiscal support.

In the ASEAN-5 countries (Indonesia, Malaysia, Philippines, Singapore, and Thailand), growth lost some momentum in the first half of 2019, due to weakening external demand. Looking ahead, growth is expected to stabilize around the mid-4 percent level.

Challenges ahead

The region’s global economic and financial integration has been an important building block underlying its tremendous economic success but, at the current juncture, it can also be a source of vulnerability. Further tariff increases and broader protectionist threats could adversely impact the region. The report finds that Asia’s investment-to-GDP ratio could be 1½ to 2 percent lower, over two years, if trade policy uncertainty were to spike and then remain at peak levels.

A related risk is that of a faster-than-expected slowdown in China. A further escalation of trade tensions could weaken external demand and depress confidence and investment. Combined with a deterioration in asset quality of financial institutions and downward pressure on property prices, this could lead to a pronounced economic slowdown with significant regional spillovers through close intra-regional linkages. A more volatile Chinese currency could also have significant regional spillover effects.

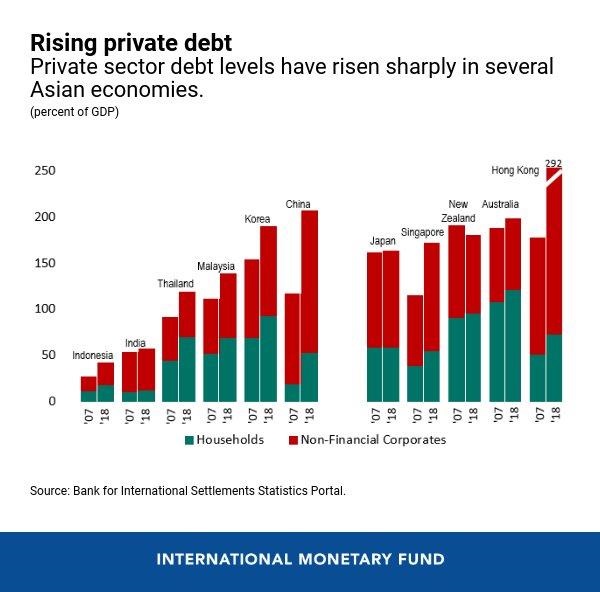

Loosening monetary policies in major advanced economies (including the United States and the euro area) are helping to soften the downturn and support favorable financial conditions. However, efforts to preserve financial stability have become more challenging amid high private sector debt and worsening corporate debt profiles. An abrupt deterioration in investor sentiment could lead to a tightening of financial conditions, with sudden capital outflows and currency depreciation. This could add further strains on corporations with weak balance sheets.

Policy priorities

Asia’s near-term policy priorities should aim at preventing a sharp growth slowdown, while reducing vulnerabilities. Efforts to diffuse trade tensions through multilateral approaches need to continue. Fiscal policy should seek to support domestic demand where this is needed and where there is policy space—for instance in Thailand and Korea. For countries like India with already high debt levels, fiscal consolidation should be prioritized to rebuild buffers. In China, additional fiscal support to cushion the impact from tariff increases would be appropriate to stabilize growth.

Monetary policy in the region can be generally accommodative, but calibrated to local circumstances. Where inflationary pressures are subdued and growth is softening—India, Korea, Philippines and Thailand—an accommodative policy is desirable. In Japan, improved market communications and further strengthening of the monetary policy framework could help lift inflation expectations.

For countries with macrofinancial vulnerabilities (such as high private sector leverage and indebtedness), it would be prudent to strengthen financial sector policies to guard against the build-up of systemic risk.

Asia needs to push ahead with structural reforms to foster resilience, while promoting sustainable and inclusive growth. Labor and product market reforms should continue (Japan, Korea, and Thailand). This includes policies to upgrade human capital (South Asia) and stimulate labor supply. Revamping infrastructure, enhancing regulatory frameworks, and further services sector liberalization can foster potential growth in the ASEAN countries. Throughout, policymakers should pay close attention to the needs of vulnerable groups to ensure that growth is inclusive. Countries should also focus on policies that incentivize lower greenhouse gas emissions, such as carbon taxes, and ensuring that they have the financial resources to meet the growing financial needs from climate change.