Asia’s strong economic rebound early this year is losing momentum, with a weaker-than-expected second quarter. We have cut growth forecasts for Asia and the Pacific to 4 percent this year and 4.3 percent next year, which are well below the 5.5 percent average over the last two decades. Despite this, Asia remains a relative bright spot in an increasingly dimming global economy.

Waning momentum reflects three formidable headwinds, which may prove to be persistent:

- A sharp tightening of financial conditions, which is raising government

borrowing costs and is likely to become even more constricting, as central

banks in major advanced economies continue to raise interest rates to tame

the fastest inflation in decades. Rapidly depreciating currencies could

further complicate policy challenges.

- Russia’s invasion of Ukraine, which is still raging and continues to

trigger a sharp slowdown of economic activity in Europe that will further

reduce external demand for Asian exports.

- China’s strict zero-COVID policy and the related lockdowns, which, coupled with a deepening turmoil in the real estate sector, has led to an uncharacteristic and sharp slowdown in growth, that in turn is weakening momentum in connected economies.

Broad slowdown

After near-zero growth in the second quarter, China will recover modestly in the second half to reach full-year growth of 3.2 percent and accelerate to 4.4 percent next year, assuming pandemic restrictions are gradually loosened.

In Japan, we expect growth to remain unchanged at 1.7 percent this year before slowing to 1.6 percent next year, weighed down by weak external demand. Korea’s growth in 2022 was revised up to 2.6 percent due to a strong second-quarter growth but revised down to 2 percent in 2023 reflecting external headwinds. India’s economy will expand, albeit more slowly than previously expected, by 6.8 percent this year and 6.1 percent in 2023, owing to a weakening of external demand and a tightening of monetary and financial conditions that are expected to weigh on growth.

Southeast Asia is likely to enjoy a strong recovery. In Vietnam, which is benefitting from its growing importance in global supply chains, we expect 7 percent growth and a slight moderation next year. The Philippines is forecast to see a 6.5 percent expansion this year, while growth will top 5 percent in Indonesia and Malaysia.

Cambodia and Thailand will expand faster in 2023 on a likely pickup in foreign tourism. In Myanmar, which has endured a deep recession due to the coup and pandemic, growth this year is expected to stabilize at a low level amid continued unrest and suffering.

The outlook is more challenging for other Asian frontier markets. Sri Lanka is still experiencing a severe economic crisis, though the authorities have reached an agreement with IMF staff on a program that will help to stabilize the economy.

In Bangladesh, the war in Ukraine and high commodity prices has dampened a robust recovery from the pandemic. The authorities have preemptively requested an IMF-supported program that will bolster the external position, and access to the IMF’s new Resilience and Sustainability Trust to meet their large climate financing need, both of which will strengthen their ability to deal with future shocks.

High debt economies such as Maldives, Lao P.D.R., and Papua New Guinea, and those facing refinancing risks, like Mongolia, are also facing challenges as the tide changes.

We expect growth across Pacific Island Countries to rebound strongly next year to 4.2 percent from 0.8 percent this year as tourism-based economies benefit from eased travel restrictions.

Inflation remains elevated

Inflation now exceeds central bank targets in most Asian economies, driven by a mix of global food and energy prices, currencies falling against the US dollar, and shrinking output gaps. Core inflation, which excludes volatile food and energy prices, has also risen and its persistence—driven by inflation expectations and wages—must be closely monitored.

Meanwhile, the US dollar has strengthened against most major currencies as the Federal Reserve raises interest rates and signals further hikes to come. Most Asian emerging market currencies have lost between 5 percent and 10 percent of their value against the dollar this year, while the yen has depreciated by more than 20 percent. These recent depreciations have started passing through to core inflation across the region, and this may keep inflation high for longer than previously expected.

Finally, spikes in global food and energy prices early this year threatened to abruptly raise the cost of living across the region, with particularly strong implications for the real incomes of lower-income households that spend more of their disposable income on these commodities.

Policy for challenging times

Amid lower growth, policymakers face complex challenges that will require strong responses.

Central banks will need to persevere with their policy tightening until inflation durably falls back to target. Exchange rates should be allowed to adjust to reflect fundamentals, including the terms of trade—a measure of prices for a country’s exports relative to its imports—and foreign monetary policy decisions. But if global shocks lead to a spike in borrowing rates unrelated to domestic policy changes and/or threaten financial stability or undermine the central bank’s ability to stabilize inflation expectations, foreign-exchange interventions may become a useful part of the policy mix for countries with adequate reserves, alongside macroprudential policies. Countries should urgently consider improving their liquidity buffers, including by requesting access to precautionary instruments from the Fund for those eligible.

Public debt has risen substantially in Asia over the past 15 years—particularly in the advanced economies and China—and rose further during the pandemic. Fiscal policy should continue its gradual consolidation to moderate demand alongside monetary policy, focused on the medium-term goal of stabilizing public debt.

Accordingly, measures to shield vulnerable populations from the rising cost of living will need to be well-targeted and temporary. In countries with high debt levels, support will need to be budget-neutral to maintain the path of fiscal consolidation. Credible medium-term fiscal frameworks remain an imperative.

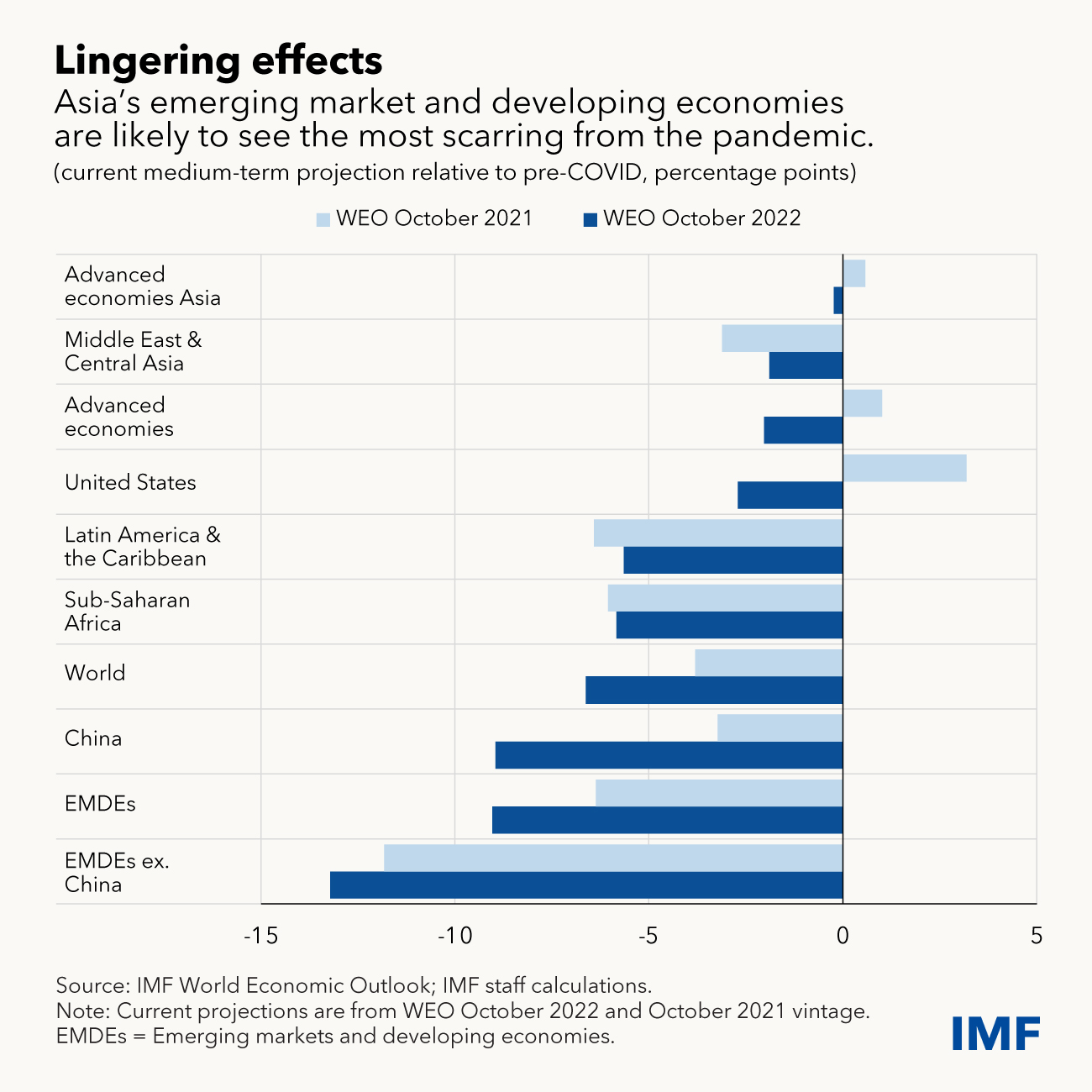

Beyond the short term, policies must focus on healing the damage inflicted by the pandemic and war. Scarring from the pandemic and current headwinds are likely to be sizable in Asia, in part because of elevated leverage among companies that will weigh on private investment and education losses from school closures that could erode human capital if remedial measures aren’t taken today.

Strong international cooperation is needed to prevent greater geoeconomic fragmentation and to ensure that trade aids growth. There is an urgent need for ambitious structural changes to boost the region’s productive potential and address the climate crisis.