Billions of consumers around the world are seeing higher oil prices seep into the cost of living and wages. Filling the gas tank soon starts to cost more when crude prices climb, as does airfare, but higher energy costs also boost prices for all the products on store shelves. Workers seek higher wages to compensate for a loss in their purchasing power.

These are what economists call second-round effects, and they can in turn further raise prices. If this feedback is large and sustained, a wage-price spiral could emerge, with wage growth and inflation rising over an extended period.

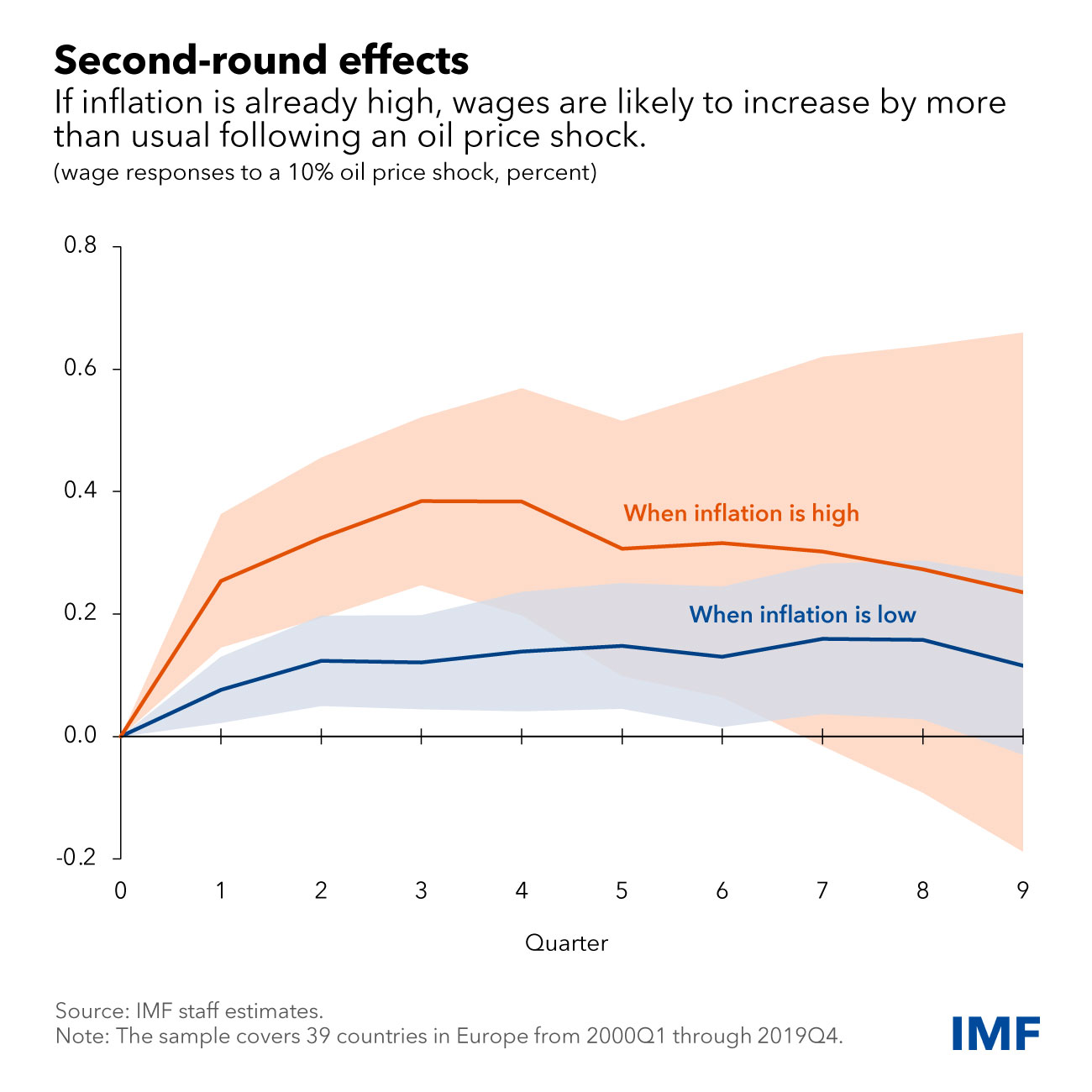

As the Chart of the Week shows, when overall inflation is already high, like it is now, wages tend to increase by more in response to an oil price shock. This finding, based on a study of 39 European countries, may reflect that people are more likely to react to price increases when high inflation is visibly eroding living standards.

The larger the second-round effects, the greater the risk of a sustained wage-price spiral through a feedback loop between wages and prices. If large and sustained, oil price shocks could fuel persistent rises in inflation and inflation expectations, which should be countered by a monetary policy response.

As our chart shows, the risk of such a dynamic tends to be greater when the overall inflation rate is already high. For example, wages increase by 0.4 percent when underlying inflation is higher than 4 percent, one year after a 10 percent increase in oil prices, but increase by less than 0.2 percent otherwise.

When overall inflation is higher, people tend to be more alert to price increases of all stripes and seek higher compensation for oil price rises. However, differences between high and low inflation periods narrow in the second year. These results impart two messages on the current situation, one concerning and the other reassuring.

Of concern is how current high inflation could increase the risk of energy prices causing sizable second-round effects an d a sustained increase in inflation, which includes pushing up inflation expectations. To head off such a risk, central banks will need to respond firmly.

What’s reassuring is the chart shows that even in a high-inflation environment, wages stabilized after a year rather than continuing to rise at a steady clip. In other words, there was a wage level but not a wage inflation increase.

To the extent that central banks remain adequately vigilant, current high inflation could still cause higher compensation for the cost of living than usual but need not morph into a sustained increase in inflation.