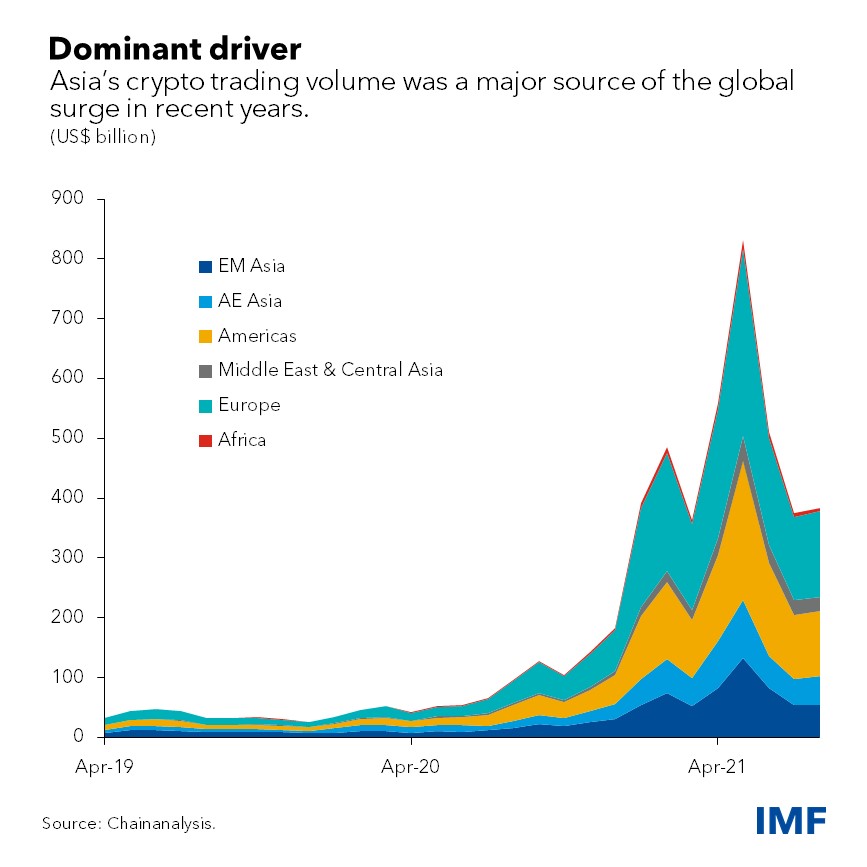

Few parts of the world have embraced crypto assets like Asia, where top adopters include individual and institutional investors from India to Vietnam and Thailand. This raises the important issue of the extent of integration of crypto into the financial system in Asia.

While digitalization can aid in the transition to an environmentally-conscious payment system and also foster financial inclusion, crypto can pose financial stability risks.

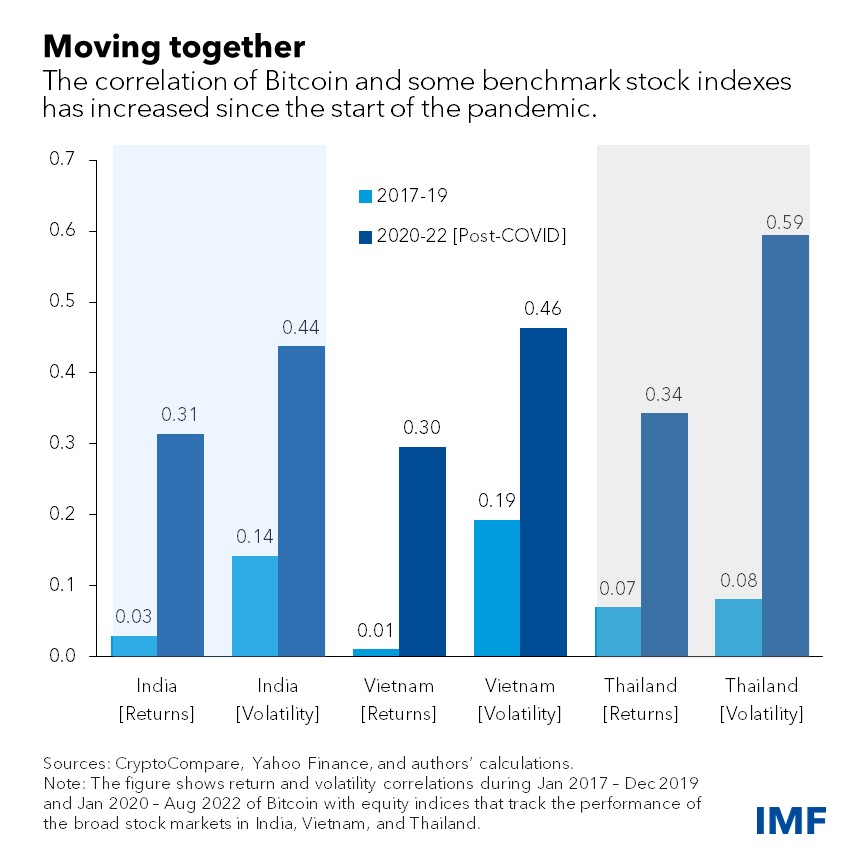

Before the pandemic, crypto seemed insulated from the financial system. Bitcoin and other assets showed little correlation with Asian equity markets, which helped diffuse financial stability concerns.

Crypto trading, however, soared as millions stayed home and received government aid, while low interest rates and easy financing conditions also played a role. The total market value of the world’s crypto assets surged 20-fold in just a year and a half to $3 trillion in December. Then it plunged to less than $1 trillion in June as central bank interest rate increases to contain inflation ended easy access to cheap borrowing.

While the financial sector appears to have been insulated from these sharp movements, it may not be in future boom-bust cycles. Contagion could spread through individual or institutional investors that may hold both crypto and traditional financial assets or liabilities. Large losses on crypto may drive these investors to rebalance their portfolios, possibly causing financial-market volatility or even default on traditional liabilities.

As Asian investors piled into crypto, the correlation between the performance of the region’s equity markets and crypto assets such as Bitcoin and Ethereum has increased. While the returns and volatility correlations between Bitcoin and Asian equity markets were low before the pandemic, these have increased significantly since 2020.

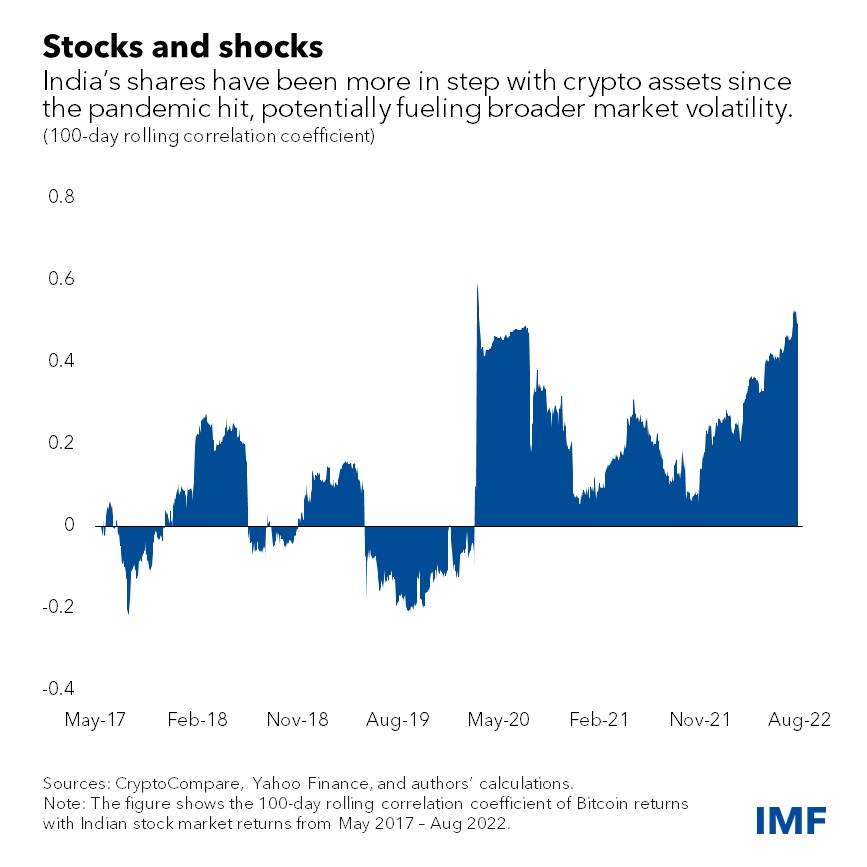

For example, the return correlations of Bitcoin and Indian stock markets have increased by 10-fold over the pandemic, suggesting limited risk diversification benefits of crypto. The volatility correlations have increased by 3-fold suggesting possible spillovers of risk sentiment among the crypto and equity markets.

Key drivers of the increased interconnectedness of crypto and equity markets in Asia could include growing acceptance of crypto-related platforms and investment vehicles in the stock market and at the over-the-counter market, or more generally growing crypto adoption by retail and institutional investors in Asia, many of whom have positions in both the equity and crypto markets.

Using the spillover methodology developed in our January Global Financial Stability Note, we also find that the rise in crypto-equity correlations in Asia has been accompanied by a sharp rise in crypto-equity volatility spillovers in India, Vietnam, and Thailand. This indicates a growing interconnectedness between the two asset classes that permits the transmission of shocks that can impact financial markets.

Accordingly, authorities in Asia are increasingly sensitive to the rising risks posed by crypto as adoption continues to spread. They have therefore dialed up their focus on crypto regulation, and regulatory frameworks are underway in several countries including India, Vietnam and Thailand.

A significant effort is also needed to address important data gaps that still prevent domestic and international regulators from fully understanding ownership and use of crypto and its intersection with the traditional financial sector.

Regulatory frameworks for crypto in Asia should be tailored to the main uses of such assets within the countries. They should establish clear guidelines on regulated financial institutions and seek to inform and protect retail investors. Finally, to be fully effective, crypto regulation should be closely coordinated across jurisdictions.